Results and trends

According to the Economist Intelligence Unit global rankins, Dubai is in the top five most comfortable cities for living in the Middle East and Africa. The city retains its status as one of the most dynamic economic centres, offering high living standards, advanced infrastructure and investments safety, which attracts buyers. A combination of the Emirate’s innovations, technological transformations and strategic location creates a benign environment for transformation of the real estate market, boosting stable growth and development in the long run.

Stable growth

The Dubai residential real estate market continues demonstrating stable growth. In Q3 2024 the volume of sales surged by 52% year-on-year with buyers still giving preference to off-plan projects. The most popular area for buying apartments was Jumeirah Village Circle (JVC), wereas the highest number of transactions with villas were made in other areas, such as The Valley, Damac Hills 2 and Dubai South.

In the meantime, the rent growth on new lease agreements neared 23% over the past 12 months. The number of transactions with apartments and villas has increased by 6% and 16% accordingly.

Robust construction and development of new areas

Vibrant development and urban regeneration is going on. New residential projects are commissioned, above all, in Meydan One and JVC neighborhoods. Overall, 19,700 new units were rolled out to the Dubai housing market in Q3 2024.

Bringing a large number of residential projects out to the market in new areas being currently developed led to the correction of the weighted average price of transactions amid the changing structure of supply and respective demand in favor of more affordable products.

Interest in branded residences

The interest in branded residences remains high. In Q3 2024, the launching of one more project, Bvlgari Lighthouse by Bvlgari, was announced.

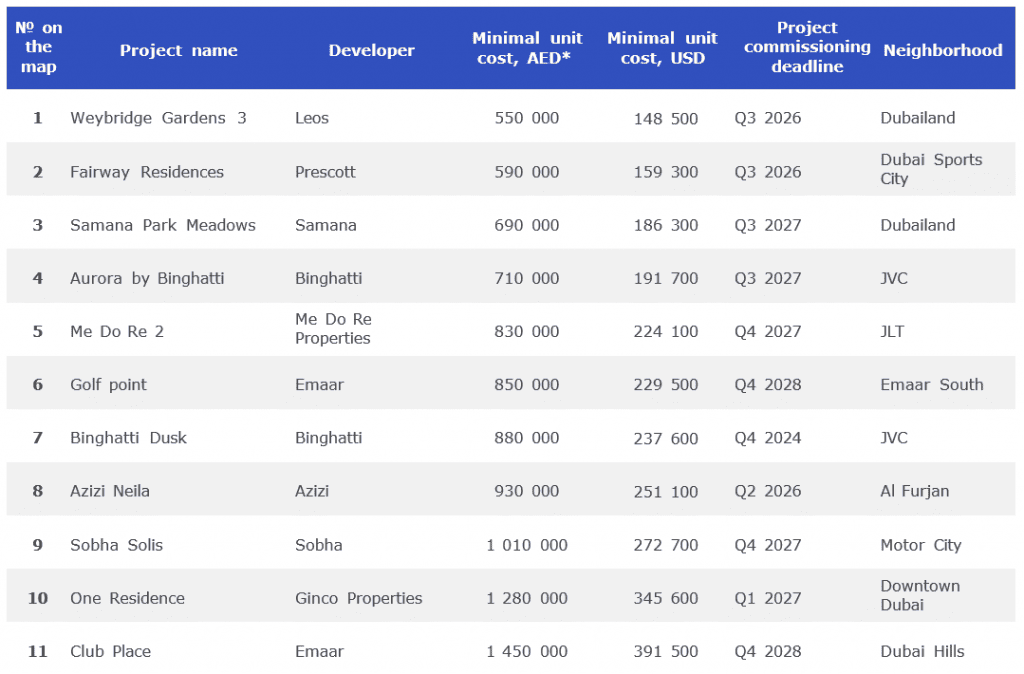

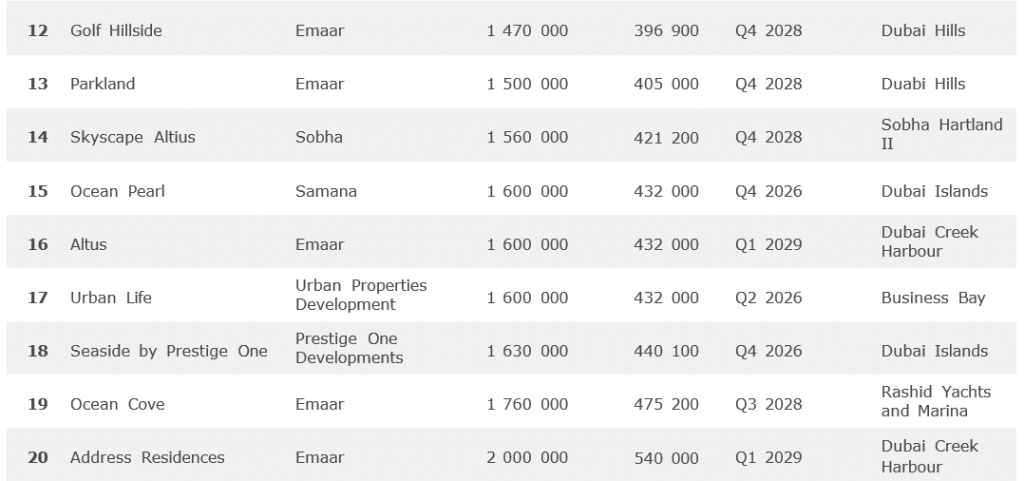

The examples of projects where sales commenced in Q3 2024

.png")

* 1 AED (1 Dirham) = 0.27 USD

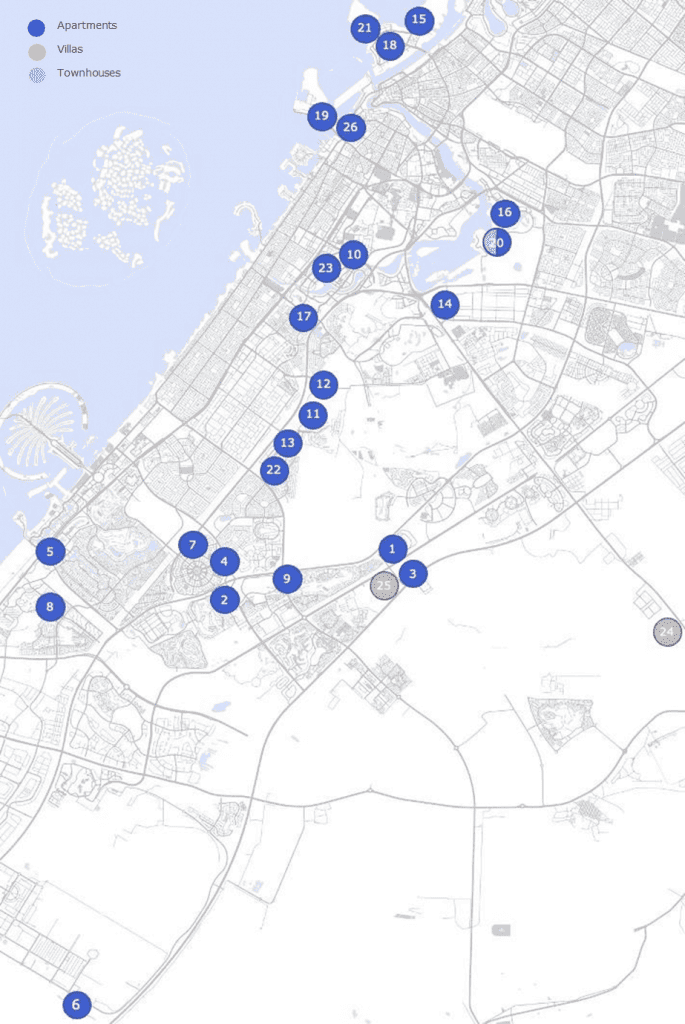

The map of sales in residential projects that got started in Q3 2024

Supply

Cumulatively, during the first 9 months of 2024, 19,700 new units entered the Dubai residential real estate market, which is 30% less than in the same period last year, with 80% of residential units being apartments and 15% - villas.

In the structure of supply by number of rooms, one-bedroom* apartments took the lead, their share standing at 33%. Studios and 2-bedroom apartments accounted for 27% and 17% of the total supply, respectively.

Dynamics of residential real estate commissioning in Dubai - Q3 2024

Dubai neighborhoods with the highest amount of commissioned housing for 9 months of 2024 (thou units)

Source: Nikoliers, REIDIN

Meydan one (part of the emerging large district MBR City) was the leader in the initial three quarters of 2024 in terms of commissioned housing. For comparison, in the similar period last year the leading positions were taken by Business Bay and Downtown Dubai. But the specifics of those areas are high land prices and a limited supply of development land, which forces developers to build new projects in other parts of the city. New points of growth and demand attraction in developing neighborhoods are emerging.

* One-bedroom apartments imply the presence of one isolated bedroom and a shared zone with a living room and kitchen.

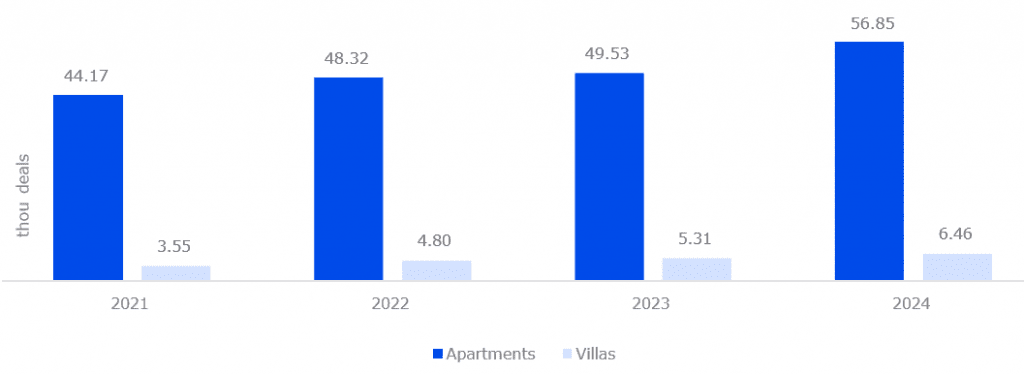

Demand

Sales in the off-plan housing market of Dubai totaled to more than 81,000 transactions, up 52% year-on-year. Transactions with off-plan housing accounted for about 92% of total deals. The supply in ready-to-move-in projects is limited and cannot compete with attractive terms from developers, which are valid only for projects under construction, such as the interest-free installment plans.

The most popular area for apartment purchase was Jumeirah Village Circle (JVC) that accounted for 25% of total transactions. The highest volume of deals with villas is concentrated in areas, such as The Valley, Damac Hills 2, Dubai South.

Dynamics of housing sales in Dubai, 2021-2024

.png")

Total transactions concluded in the market of housing under construction for 9 months of 2024 (by neighborhoods, number of deals)

Source: Nikoliers, REIDIN

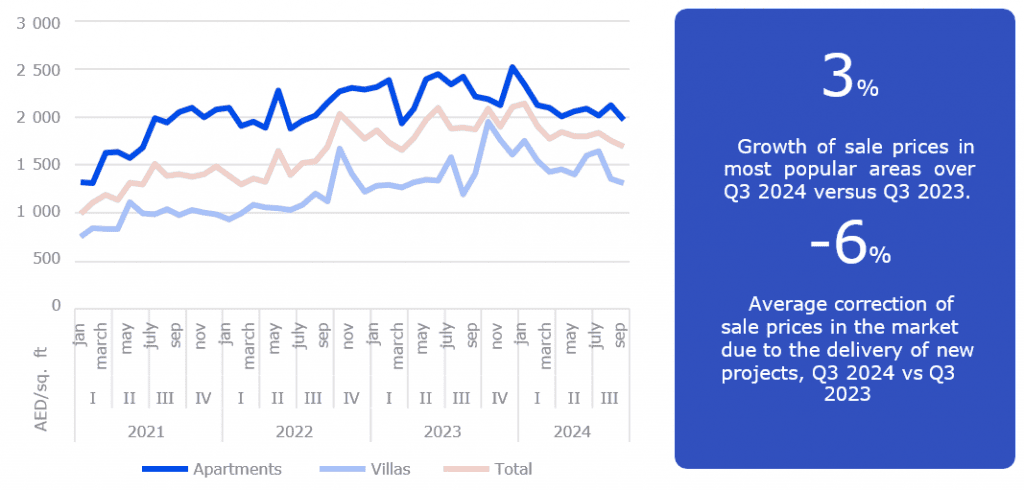

Sale prices

As per the General Plan of Dubai Development, city aims at increasing its population to 6 million people by 2040. This trend will whip up demand for housing purchase and rent. As of the end of Q3 2024, the weighted average price per sq. ft in off-plan housing projects averaged AED 1,771 (USD 5,147 per sq. m) - 6% less than in Q3 2023. The price correction has to do with changes in the supply structure due to sales launched in the projects developed in new neighborhoods where housing prices are way lower than in more developed areas.

In the most popular areas, such as Business Bay, Downtown, Dubai Marina, JVC, Damac Hills, we can see a stable growth of prices. The weighted average price per sq ft in those five neighborhoods amounted to AED 2,192 per sq. ft (USD 6,386 per sq. m) in Q3 2024, up 3% year-on-year.

Dynamics of the weighted average price in the off-plan housing market of Dubai, 2021-2024

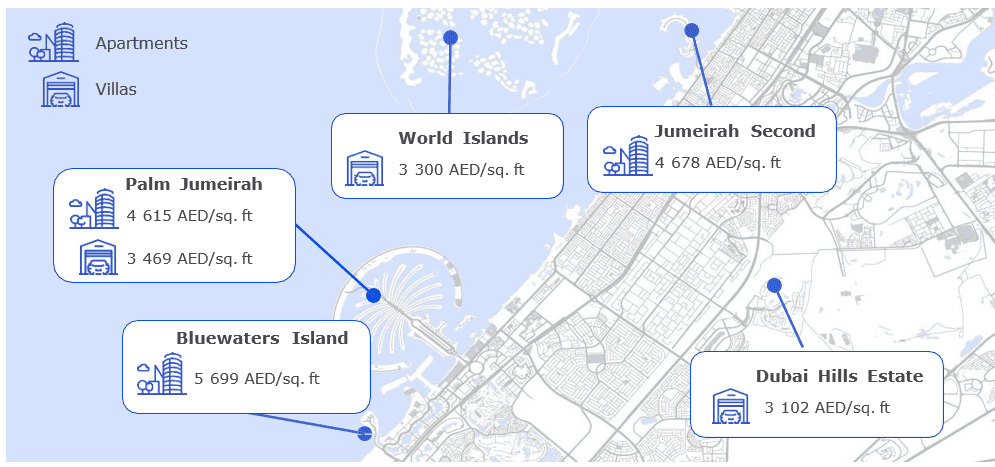

The most expensive offers per sq. ft of apartments in Q3 2024 were concentrated in the following neighborhoods: Bluewaters Island, Palm Jumeirah, Jumeirah Second; for villas these are World Islands, Palm Jumeirah and Dubai Hills Estate.

The map with most expensive neighborhoods in terms of weighted average price per sq. ft of real estate, Q3 2024

Source: Nikoliers, REIDIN

Rent

Over 9 months of 2024, as compared to a similar period in 2023, the number of new lease agreements for apartments has risen by 6%, while for villas the growth was 16%.

Dynamics of new lease transactions in Q3 of 2021-2024

In the rental market we can observe growth in quantitative and price indicators. Thus, over the last 12 months the growth of rental rates on new contracts in Dubai amounted to about 23%. In the most popular areas - JVC, Business Bay, Damac Hills 2 - the growth of rental rates was lower than the market average (10%) due to a large number of offers in the midst of rampant housing commissioning during 2023-2024. Current tenants prefer to renegotiate existing leases, as this allows them to maintain the already agreed terms and avoid significant increases in rental costs due to legislative restrictions.

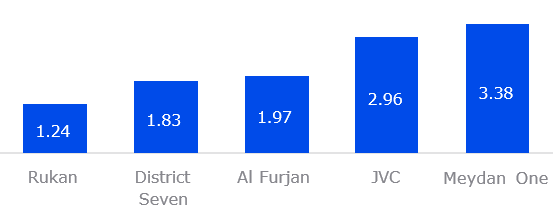

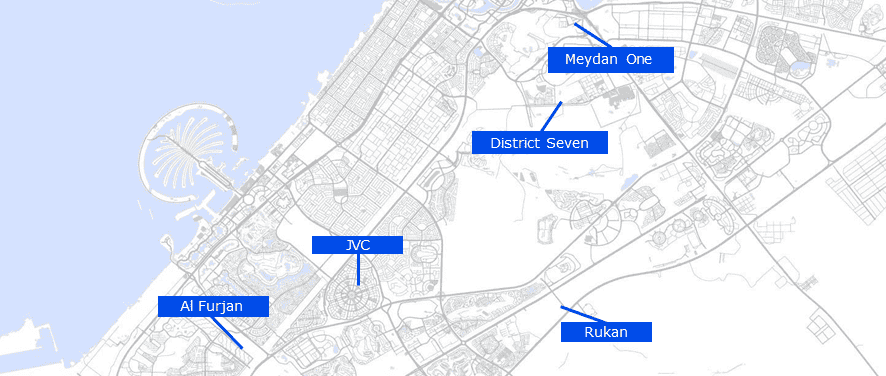

Neighborhoods with the highest number of signed new lease agreements in Q3 2024 (thousand contracts)

(1).png")

Source: Nikoliers, REIDIN