Key factors that influenced the Moscow market of new builds in Q3 2024*

The key rate rise to 19% enhanced the attractiveness of deposits,/span>

In Q3 2024, the Bank of Russia’s Board of Directors raised the key rate twice (on July 26 to 18% and on September 13 to 19% per annum). Increases in the refinancing rate make mortgages on market terms unaffordable for the majority of the population, drawing capital to savings accounts. As of October 1, 2024, there was a record volume of household deposits reaching RUB 51.1 trillion, which is almost half of the country’s total money supply.

New terms of preferential mortgage programs

In July-September 2024, the terms for family and IT mortgage loans underwent changes. The program for families with children was extended until 2030, but the interest rate rose to 6%. In July, the conditions for the age of children were tightened: now the family mortgage can only be provided to families with a child younger than 7 years old, and in September, a number of banks raised the down payment to 50%, which narrowed the circle of borrowers. IT-mortgage under the new terms is not available for buying housing in Moscow or St. Petersburg.

Exhaustion of limits

Despite the extension of the family mortgage program until 2030, already at the end of September 2024 most banks ran out of limits to the main driver of demand for the mass-market real estate segment. The Central Bank announced that it will redistribute the remaining limits among banks. It is expected that the terms of both preferential programs (including under the IT-mortgage program) will be revised soon, but at the moment the almost complete exhaustion of limits slows down the dynamics of transactions.

* Hereinafter in this report the data are provided for residential units and apartments within the boundaries of “old” Moscow with elite real estate excluded.

Results of Q3 2024 and forecasts for the Moscow market of new builds*

Multidirectional dynamics of prices

Over the quarter, the weighted average price for all classes of residential real estate showed an 1.8% growth (to RUR 516,000 per sq m), due to an increase in the weighted average prices of business and premium classes (price growth over the quarter by 3% and 2%, respectively). On the contrary, in comfort class there was a 1.6% price decrease quarter-on-quarter (and 2% year-on-year).

The number of lots on offer has grown

Developers continue to put new living space on sale, including in recently launched projects. There are 49,700 residential units and apartments (or 2.77 million sq m) in exposure. An increase in the number of lots amounted to 7% over the quarter. Developers are buildng up the living space in open exposure, including due to a larger number of one-room units, i.e. with minimal transaction value.

The demand has slowed down, housing mortgage loan denials have become more frequent, the share of mortgage in transactions has gone down by 17 p.p.

In Q3 2024, there was a 24% decrease in the number of registered shared-equity agreements as compared to the previous quarter and a 36% decrease vs. the previous year. Several factors contributed to flagging demand, the key one being the completion of the preferential mortgage program with state backing. Changes in the terms of family and IT-mortgage, exhaustion of limits in most banks on preferential mortgage programs, increase in the down payment to 50% (by some of the lenders), seasonal decline in buying activity during summer months were other factors. According to the National Bureau of Credit Scores, the share of rejected mortgage applications (denial rate) reached a historic high of 57% in July 2024.

Instalment plans are getting increasingly popular

Developers are rapidly expanding their line-up of installment plans, both varying the size of the initial instalment and providing a longer period (with or without an increase in the price of the unit, with full payment for the period of installments or with the ability to repay the balance in a single payment by the time of receiving the commissioning permit, with monthly or quarterly payments and the ability to switch to a housing mortgage loan at any time, etc.). This allows a potential buyer possessing an amount equivalent to the full value of the property, both to earn off a deposit in the horizon of 2-3 years, and to become the owner of a lot under construction, buying it in installments from the developer.

Introduction of the “mortgage standard” starting in 2025 has been announced

The Ministry of Finance together with the Bank of Russia have developed and approved a mortgage standard, which will become effective from the beginning of 2025 and will regulate the mortgage market to form the rules and norms of interaction between market participants. The innovation is caused by the fact that currently developers in cooperation with banks offer subsidized rates with more favorable mortgage terms, which, in turn, entails an increase in the cost of purchased housing.

* Hereinafter in this report the data are provided for residential units and apartments within “old” Moscow and elite real estate is excluded. The analysis covers comfort, business and premium housing classes.

New projects launched

Total supply in open sale increased by 5.8% in Q3 to 2.77 million sq m of residential units and apartments. Compared to last year, the increase amounted to 11% (2.49 million sq m). Developers offer 49,700 lots for sale, up 7% more versus the previous quarter and 11% more than last year.

The total new supply in exposure in Q3 2024 is 13% lower than in the previous quarter (200,000 sq m). At the same time, the total living space in projects (by PDs) launched in the current quarter exceeds the last year’s figure by 7% (1 million sq m) amounting to 1.1 million sq m.

The growth rates of weighted average housing price slowed down by the end of Q3 2024. That being said, the price decrease in the comfort class was 1.6% per quarter and 2% per year. Business and premium housing classes, on the contrary, have the potential for growth in value even in the unstable economic environment (during the quarter the price growth in business class amounted to 3%, in premium class - to 2%).

The number of registered shared-equity agreements went down by 24% during the quarter (over the year - by 36%) amounting to about 722,000 sq m of sold lots.

The average area of sold lots increased by 2 sq m from 50 to 52 sq m due to changes in the structure of demand and in the demand for large-sized lots (2-room, 3-room, 4-room units), which clients buy increasingly often for cash or using installment plans.

Demand and supply dynamics

Source: Nikoliers, exlusive of elite real estate

|

87% |

The share of residential units in the supply by real estate type (a 1% increase versus Q2 2024). |

The structure of housing supply by classes did not show any significant changes over the quarter. Business and comfort segments dominate the sales offer (each accounting for more than 40% of the total supply).

In Q3 2024, almost half of the total supply consisted of one-room residential units and apartments (45%). This indicator almost doubled during the quarter (from 28%). In order to quickly fill escrow accounts, developers put lots with lowest budgets of a potential transaction on sale.

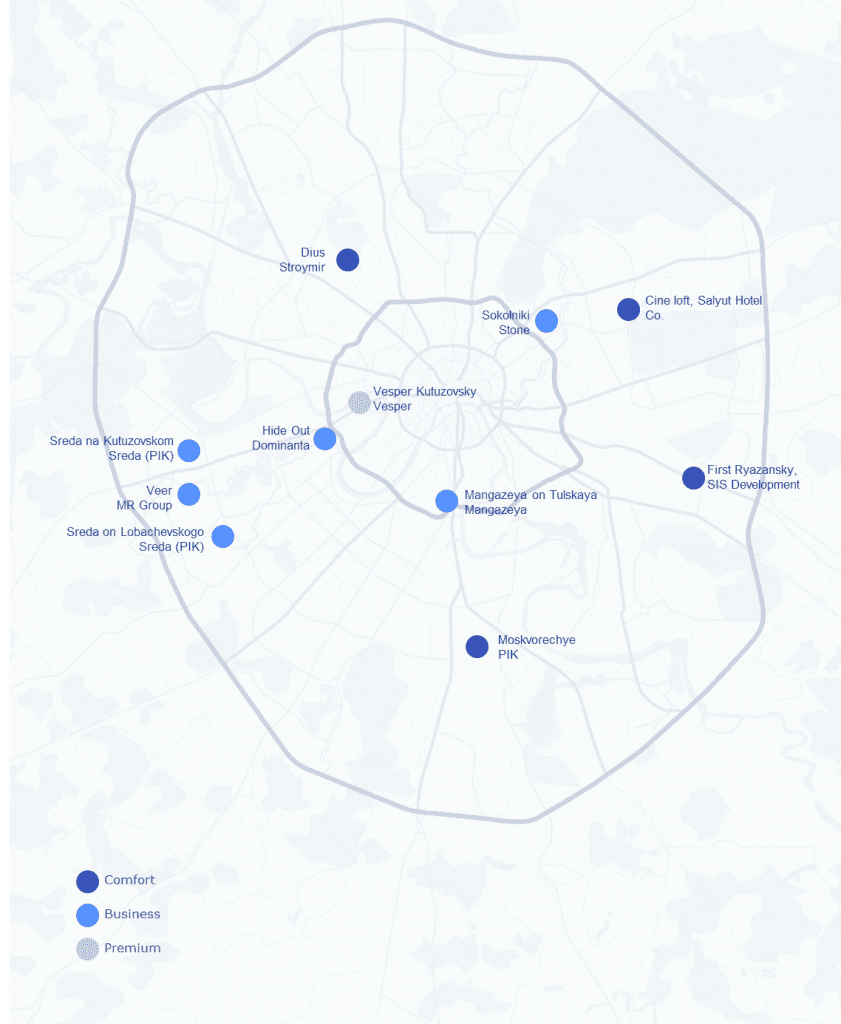

The largest supply is concentrated in the South and West of Moscow (16% each). These districts hold the leadership in terms of exposure for the third quarter in a row since the beginning of 2024.

Based on the results for Q3 2024, the main bulk of supply in South Moscow is represented in the Wave project by LSR (44,900 sq m), including due to the roll-out of new buildings of the 2nd phase. The project in West Moscow with the widest exposure is Luchi-2 by LSR (58,000 sq m).

Supply structure

Source: Nikoliers, exclusive of elite real estate

Prices

Weighted average price dynamics

Based on the results for Q3 2024, the weighted average price in comfort class decreased by 1.6% quarter-on-quarter and by 2% year-on-year. Due to the adjustment of demand in the midst of prohibitive interest rates in housing mortgage programs and a slump in purchasing activity, developers started rolling out new space at a discount to the market; in the meantime prices in their projects are growing in accordance with the underlying model. The overall increase in the weighted average price for all classes amounted to 11% in annual terms and to 1.8% in quarterly terms.

Central Moscow remains the most expensive district of the capital city both for residential units and apartments. Thus, if the price of a residential unit has risen 5% in Central Moscow over the quarter (from RUB 870,000 per sq m to RUB 911,000 per sq m), the price of apartments, on the contrary, has dropped by 5% there. The price per square meter of residential units was affected by the price adjustment in the projects already on sale (Life Time by Sminex - 10%, Luzhniki Collection by Absolut - 9%). As for apartments, developers reduced prices for projects on sale as well: the most significant decrease over the quarter was in the Cosmo 4/22 project by Hals Development (10%) and Dolgorukovskaya 25 project by Bell Development (9%).

Weighted average price by districts, RUB thou per sq m

Source: Nikoliers, exclusive of elite real estate

Demand

|

94% |

The share of residential units in the structure of demand by real estate type (down 1 p.p. vs Q2 2024) |

According to the results of Q3 2024, more than 13,000 shared-equity agreements totaling to 722,000 sq m were registered within the boundaries of the “old” Moscow. Demand for the quarter sagged by 24%, for the year - by 36%. Such a decline is the effect of the state-backed preferential mortgage program completion (at the interest rate of 8%) and changes in the terms of the remaining preferential programs. Exclusion of IT-companies registered in Moscow from the program of preferential IT-mortgage also led to sinking demand.

The share of apartments in total sales in Q3 2024 increased (+1 p.p. per quarter) to 6%. This demonstrates the increased interest of buyers in investment-grade lots, which are cheaper than apartments (the gap in price is 4% at the end of the current quarter). This trend is especially indicative amid reduction in the share of apartments in the supply and their gradual disappearance as a separate product.

Business class is in highest demand with buyers accounting for more than half (51%) of all quarterly sales (increase in the share by 4 p.p. per quarter).

In Q3 2024, the demand for studios with the minimum transaction amount is stable, but despite the growth of 1-room lots in the supply, their share in total demand has contracted (by 5 p.p. over the quarter, from 40% to 35%). Customers increasingly often buy large-sized residential units paying 100% of their cost in cash or using installment plans.

The leader in sales in Q3 2024, like also a quarter earlier, was Moscow West with the share of 20% from total sales in Moscow. The demand in the Western District exceeds the supply (16% in total exposure). The best-selling project in Moscow West was Luchi-2 by LSR, where 344 lots of more than 10,000 sq m were sold in Q3. In the Southern District the largest number of lots was sold in Shagal by Etalon (334 co-invetsment agreements totaling to about 19,000 sq m).

Structure of demand by payment type

|

17p.p. |

The shrinking share of mortgage-backed transactions for Q3 2024 amid changes in the terms of issue under preferential mortgage programs (from 73% to 56% over the quarter). |

Structure of demand

Source: Nikoliers, exclusive of elite real estate