Main results

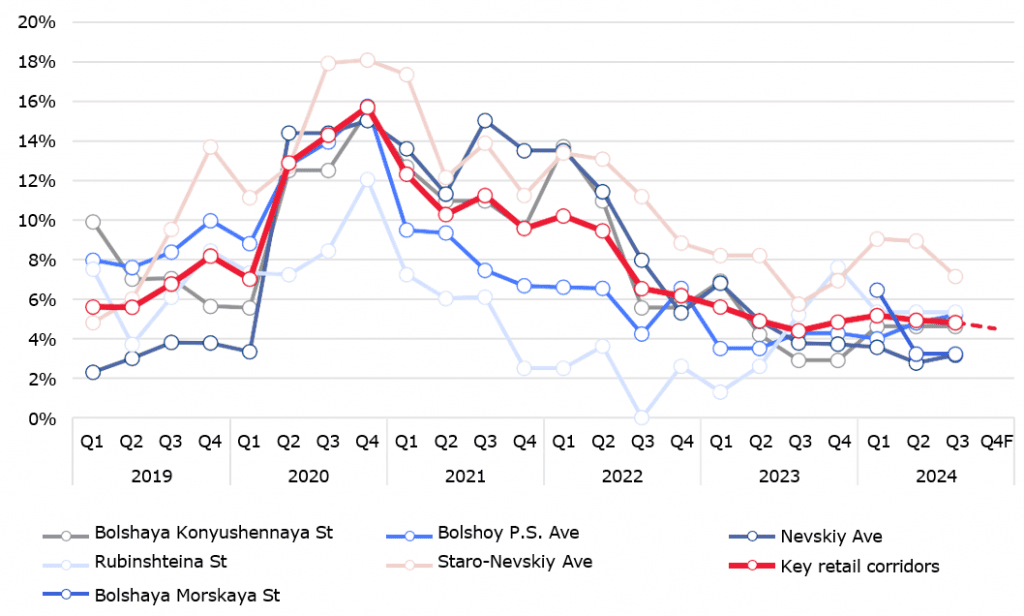

In the third quarter of 2024, the average vacancy rate on the main retail routes or corridors of St. Petersburg dived by 0.2 p.p. relative to the previous quarter to 4.7% by the end of September. Thus, this indicator has approached its all-time low for five recent years. By the end of 2024, the vacancy rate is expected to stabilize at the level of 4.5%.

A radical reduction of the vacancy rate took place only on Staro-Nevsky Ave, where this indicator dropped by 1.8 p.p. The change in vacancy has to do with the simultaneous opening of several catering outlets as well as clothing shops which replaced the foreign brands that left the market. No substantial changes in the vacancy rate was recorded on other retail routes.

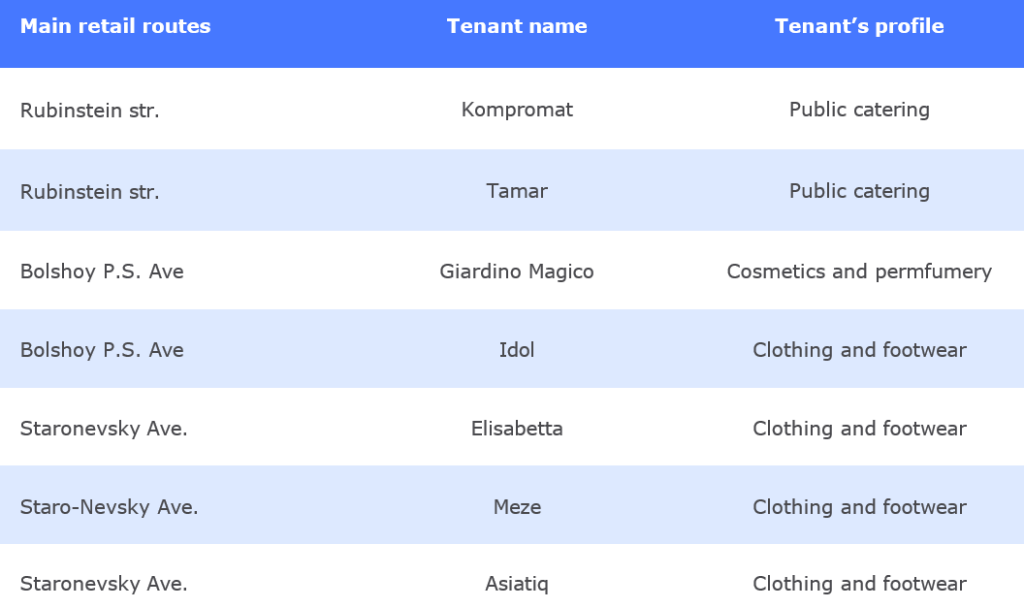

Public catering that was responsible for the lion’s part of all openings on the main retail streets of St. Petersburg in the third quarter is still one of the key segments in terms of activity. Among the most interesting projects is the Turkish restaurant Meze and the Asian cafe Asiatiq on Staro-Nevsky Ave., as well as the Tamar cafe of the Georgian cuisine and Kompromat bar on Rubinstein street.

Russian retailers open their outlets replacing foreign fashion brands that had waved good-bye. Thus, the premises of France-based Iro on Bolshoy Ave. of Petrograd will soon be occupied by Russia’s Choux, while the Russian brand of women’s clothes Elisabetta will soon take the place of the Turkish brand Ketroy that made its debut on Staro-Nevsky Ave. at the turn of the year.

Dynamics of the vacancy rate on the key retail routes, Saint Petersburg

Source: Nikoliers

Demand and commercial terms

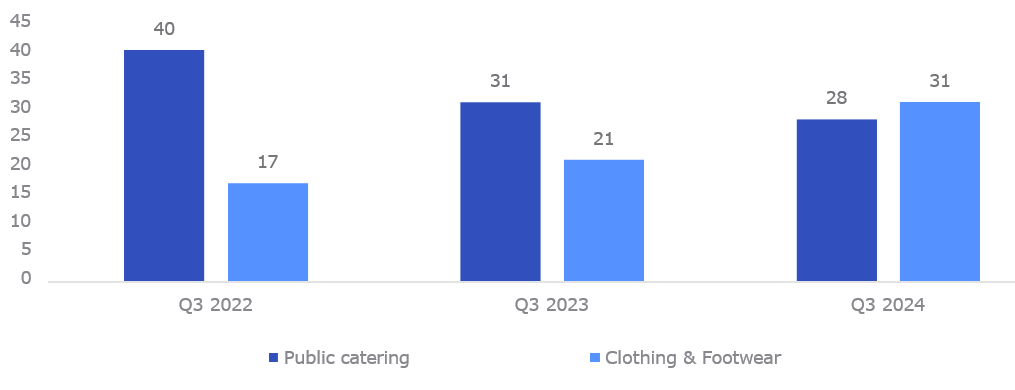

Overall 76 openings took place during the initial nine months of 2024 on the key street retail routes of St. Petersburg versus 71 openings for the similar period in 2023, with 68 closures recorded versus 62 a year before. This dynamic may well be attributed to the natural tenant rotation.

The catering segment is a traditional leader of the last three months in terms of openings, having contributed 35% of all new tenants. Yet, based on the results for 9 months of 2024 Clothing and Footwear ranks first with 41% of total openings. Whereas prior to 2022 catering had always been ahead of fashion by the number of new openings, the gap between these two segments started shrinking in three recent years due to growing popularity of fashion operators in the street retail sector - mainly local brands that have been expanding more aggressively than major chain brands. Some examples of these local brands include macrocosm, Suborbia, Le Journal Intime, Nikita Yefremov et al.

During the three quarters of 2024, fashion retailers most often picked premises on Staro- Nevsky Ave. and Bolshoy P.S. Ave with 23 new shops having opened its doors there since January (In Trend, Latrika, Estego and others). In the meantime, catering outlets still occupy street retail spaces on Nevsky Avenue and Rubinstein Street - for nine months of 2024 the total of 20 openings took place in those very locations (Open People, The Byk, Mussel Place, etc.).

The number of openings on the key retail routes in Q3 2022-2024, by segments

In Q3 2024 the quarterly rotation stood at the meager 1.9%. This low level can be explained by the fact that most retailers picked the premises, which had been reckoned as vacant for more than a quarter, for their openings.

The most vibrant tenant rotation was taking place on Nevsky and Staro-Nevsky avenues. On Nevsky Ave. the rotation is due to high competition, the split of some spaces into small-sized units as well as to high rental rates. On Staro-Nevsky Ave the tenant rotation mostly occured within one segment because of the previous tenant exiting the market or failing to make enough profit. Thus, Tedix cafe opened in place of ChaPanda cafe, while the Ketroy clothing brand replaced Elisabetta.

Average ranges of rental rates for premises for lease with floor areas from 100 to 300 sq m in Q3 2024, RUB/sq m/month, exclusive of VAT

.png")

Source: Nikoliers

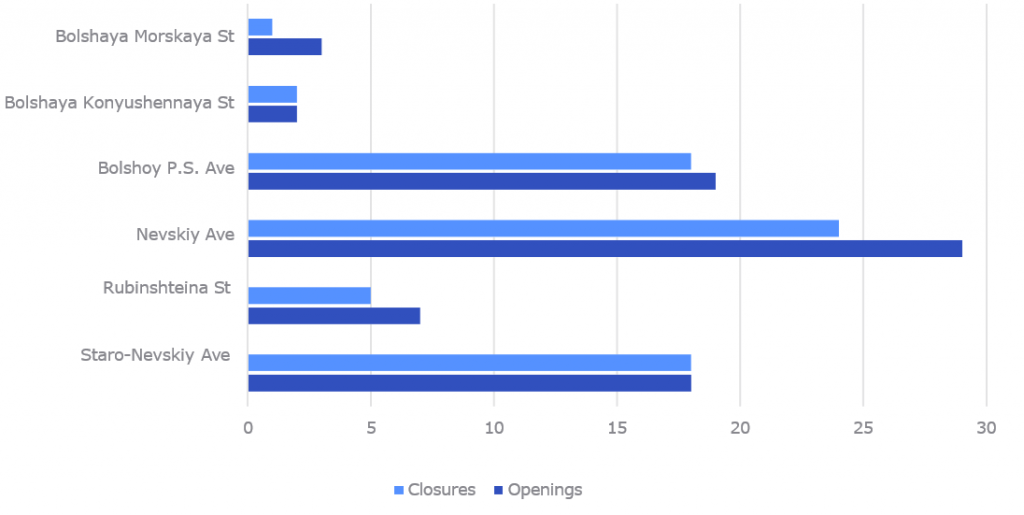

The number of opened and closed premises on the key retal routes of Saint Petersburg for Q1-Q3, 2024

On Staro-Nevsky Ave and Bolshaya Konyushennaya str. the number of closures exceeded the number of openings in H1 2024. Yet in the third quarter the openings and closures indicator went back to positive dynamics because new retailers occupied the vacated premises. For instance, Khlebnik bakery opened in the premises of AV Daily at 142, Staro-Nevsky Ave, after the latter had been closed in spring. On all the streets under review openings either exceed closures or are on a comparable level.

Key openings on the main retail routes of Saint Petersburg in Q3 2024

Source: Nikoliers

Trends and forecast

In the period of Q3 2023 to Q3 2024 we’ve seen the vacancy rate being stabilized at the level of 4-5%. The number of vacant premises on the main retail routes fluctuates in the range of 35-45, of which more than one-fourth are accommodated in the basement. Most likely, the shortage of quality premises will still be acute till the year’s end.

The replacement of foreign brands that exited the Russian market by new representatives of street retail has almost completed on the key retail thoroughfares of St. Petersburg. Very few shops once in possession of foreign brands have retained their signs, albeit being closed. One example is Prada on Bolshaya Konyushennaya Street; another one is Brunello Cucinelli on Staro-Nevsky Ave. The premises of the retailers which have left the market are mainly occupied by new actors of the same segment.

For example, the multibrand Babochka has opened in the premises once occupied by Chanel on Staro-Nevsky Ave.

The activity of fashion retailers keeps growing – the share of clothing and footwear shops amounted to 41% of all openings at the end of Q3 2024 versus 29% for the similar period in 2023. The most popular streets for fashion brands during the initial 9 months of the year were Staro-Nevsky Ave. and Bolshoy P.S. Ave.

Nevertheless, the tenant mix remains stable in 2024: catering establishments occupy 36% of all premises, fashion retailers - 21%, the rest of the segments accounting for 41% of available street retail space. No changes in these shares are expected in the foreseeable future.

Key market indicators

*The number of retail premises can change as the sample changes (some premises being consolidated under major tenants).

Source: Nikoliers