Main trends and market indicators for 2024

Market indicators

*As estimated by Nikoliers.

The Moscow metro area includes Moscow and Moscow Region within the Central Ring Motorway (CKAD). The St. Petersburg metro area includes the city of Saint Petersburg, Murino and kudrovo..

** The methodology of assessing per capita retail space in Saint Petersburg was altered in 2024: the data for Murino and Kudrovo were included.

Source: Nikoliers

Supply: Moscow area

In 2024, the new construction in the Moscow metro area came to 173,500 sq m in 13 projects. The new supply was represented only by small-sized shopping centers. In 2025 the marketing of “regional” scale projects is expected, such as an SC within Seligerskaya transfer hub (GLA=58,000 sq m).

As has been announced by developers, in 2025 the new supply may reach the level of 620 thou sq m. Yet, in our estimation, the commissioning won’t exceed 361,000 sq m of gross leasable area and will mainly comprise the projects whose grand opening dates have been postponed several times. The average floor space of the projects to be commissioned next year may rise by 13% to 15,031 sq m.

Only a third of the new supply will be classic shopping centers (e.g. Sreda Tsaritsyno SC), with 24% of new retail venues to open within mixed-use centers (e.g. a MUC as part of Ostafyevo residential development in New Moscow), 31% - within transfer hubs (such as Portal SC as part of Nizhegorodskaya transfer hub), and 11% - in stylobates of residential projects (for example, Megalit SC in the stylobate of Olymp residential development in the city of Korolev).

Dynamics of retail space commissioning in the Moscow area

*As estimated by Nikoliers.

**Part of the new Olimpiysky complex will open in 2025, but it’s only in 2026 that it will start operating in a full-scale regime.

Source: Nikoliers

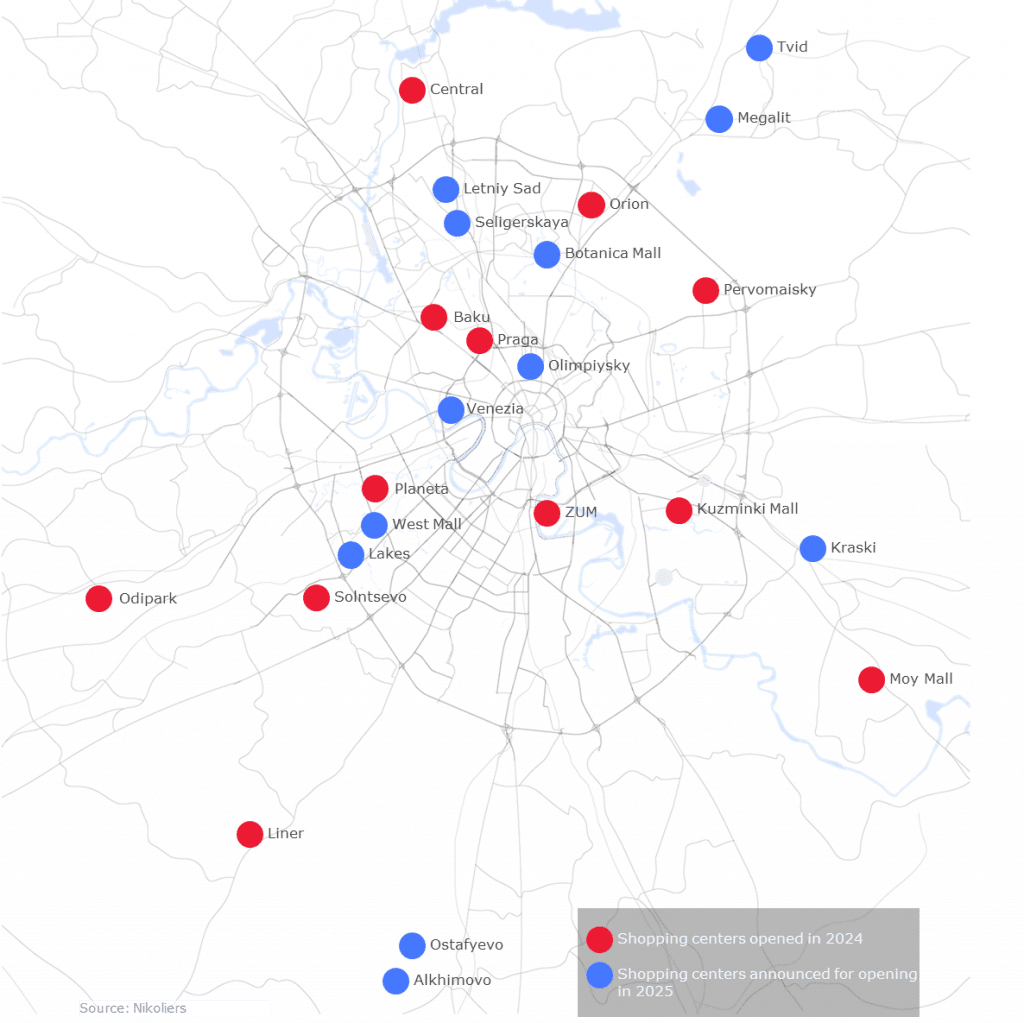

Key shopping centers, Moscow metro area

Supply: Saint Petersburg

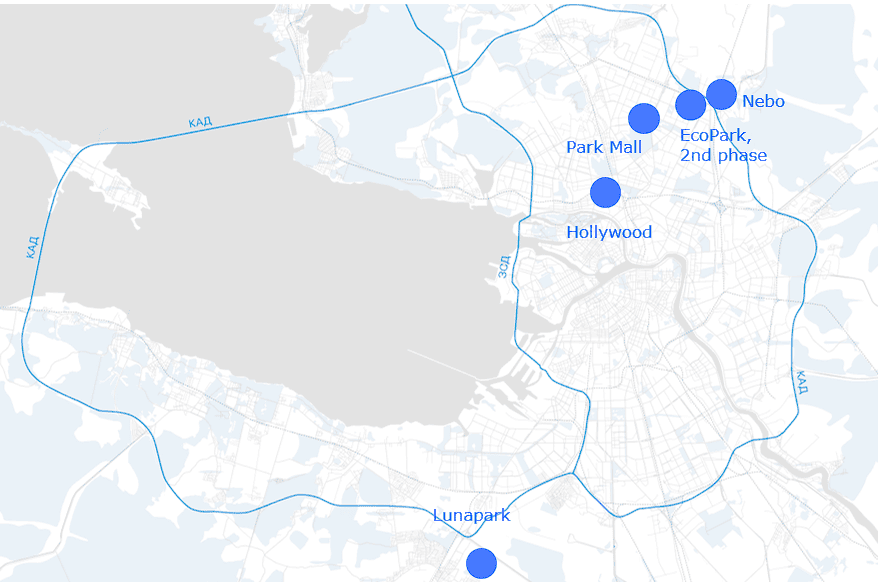

In 2024, no new retail premises have been added to the St. Petersburg market. Earlier, four new shopping centers were expected to be opened (Park Mall, Nebo shopping mall in Murino, Lunapark shopping mall in Novogorelovo, shopping mall in Kolpino), as well as the second phase of Ecopark shopping mall in Murino, which opened at the end of 2023; however, the delivery dates for all facilities have been adjusted and pushed back to 2025. Thus, St. Petersburg set a new anti-record in terms of space commissioning for the first time since 2000. Taking into account the postponement of commissioning dates, the commissioning of new retail space may amount to more than 139,000 sq m, which is a record high for the last 10 years. HOLLYWOOD mixed-use shopping mall will be the largest project among those slated for opening. Its GBA will amount to 115,000 sq m, with GLA reaching 60,000 sq m.

Shopping centers to be commissioned in 2025 by format

The HOLLYWOOD mixed-use shopping mall will be the only facility of regional scale in 2025, its floor space accounting for 46% of total retail space to be commissioned. At the present moment regional centers occupy 15% of total retail space in the St. Petersburg metro area. It was back in 2016 that the last classic shopping center with GLA in excess of 50,000 sq m was opened in St. Petersburg.

New concepts in shopping centers

Despite the zero commissioning of retail space, new concepts continue to appear in existing SCs. For example, the first Sela shop with its own cafe inside opened in Okhta Mall, whereas in Galeria Mall the cosmetics shop Zolotoye Yabloko launched a pre-holiday pop-up stand. There is an ongoing development of gastronomic spaces in shopping centers. In September 2024, the first in Murino food hall GastroPark opened in EkoPark shopping mall, while in October a gastro space appeared in Rumba SC. Several more gastro-projects are scheduled for opening in St. Petersburg during 2025. Among them is the renovated area of the former food court in the Pik shopping mall as part of that project reconception, as well as a food hall and restaurant area with open terraces along with a shared lounge space in the HOLLYWOOD mixed-use shopping mall. Park Mall announced the launch of its own online marketplace on its official website. The project is expected to open in March 2025.

Dynamics of retail space commissioning in classic and specialized shopping centers of Saint Petersburg metro area*, sq m

Projects announced for opening in Saint Petersburg metro area* in 2025

*The Saint Petersburg metro area comprises the city of St. Petersburg, Murino and Kudrovo.

Source: Nikoliers

Supply: Regions

Based on the results for 2024, the new supply in Russia, excluding the Moscow and St. Petersburg metro areas, totaled to 210,000 sq m, which was 44% higher than in 2022, but at the level of 2023. Standing out among the remarkable openings are Puzzle shopping mall in Pyatigorsk (GLA=30,000 sq m), Lyubimovo Mall in Krasnodar (GLA=27,800 sq m), Lev shopping mall in Penza (GLA=22,500 sq m).

According to our estimates, next year the retail space commissioning is expected to grow one and a half times up to 315,000 sq m. Yet big cities (with the population of over half a million) will account for 60% of all openings, cities with the population of 300-500 thousand - for 11%, cities with the population of 100-300 thousand people - for 14%, whereas towns with populations below 100,000 will account for the rest 15%.

Next year, the greatest increase in per capita retail space among the million-plus cities will be demonstrated by Yekaterinburg (+90 sq m per 1,000 residents), Krasnodar (+29 sq m per 1,000 inhabitants), Rostov-on-Don (+22 sq m per 1,000 dwellers) and Perm (+21 sq m per 1,000 people). The top three cities with the least per capita retail space will remain unchanged - only their sequence will change compared to the end of 2023: Perm, Omsk and Volgograd.

Retail space commissioned in Russia

*As estimated by Nikoliers

Source: Nikoliers

In 2025 the new supply in Russian regions will consist of small-sized SCs. Regional and superregional centers will show up in the new construction plans no sooner than in 2026. The new construction by poject type is more conservative than in Moscow, with 93% of all supply falling to the share of classic SCs.

At the end of 2025, the new high-quality retail space supply in Russia may come to 815,000 sq m, with the Moscow area accounting for about 44% of commissioned space, regional cities of Russia - for 39% and the St. Petersburg metro area - for 17%.

*As estimated by Nikoliers

Source: Nikoliers

Demand

*A brand is considered to be new:

1. If it has opened its first shop in an SC or as part of street retail, even if this is not this brand’s first entry to the Russian market.

2. If it had early been represented online or as a corner (pop-up) shop in a departmnt store and then made its debut as a monobrand boutique.

**Already closed.

Source: Nikoliers

Tenants of shopping centers

Grocery retail

The size of grocery stores in shopping centers keeps dwindling. The E-grocery segment is rapidly growing with grocery retailers expanding their coverage areas, reducing the time of delivery and developing an omni-channel approach.

Public catering

Food halls continue opening at the premises of shopping centers as the given concept enables to breathe in new life into SCs and increase attendance. Tenants in the catering category willingly and rather successfully collaborate with fitness and fashion.

Sporting and wellness goods

The market of sporting goods has lost a lot of major foreign brands for several recent years, which opens opportunities for new players to fill the given niche. The Italian sports clothes brand Carra is expected to enter the Russian market in 2025. Joint collaborations of Fitness and Sportng goods operators spur further expansion of this segment.

Clothing and footwear

The expansion of Russian and foreign brands is slowing down. Fashion retailers will improve the design of their points of sale while also venturing on cooperation with brands of other profiles. Ineffective spaces are being vacated, which may entail an insignificant growth of vacancies in shopping centers.

Entertainments

The cine industry has not fully recovered. It continues adaptation to low content flows, focusing on small hall sizes and developing VIP services.

Many landlords and management companies are shifting their focus towards entertainments for teenagers and adults, with bowling, VR spaces, cyber sporting networks picking up pace.

Footfall: Moscow

The attendance of shopping centers in Moscow has grown by 1.8% during 11 months of 2024 versus 11 months of 2023. The SC footfall for January-November of 2024 exceeded the results for a similar period of 2022 by 0.7%. Nevertheless, this indicator is still 5.9% behind its value in 2021. In 2025 the footfall in Moscow SCs is projected to match the level of 2024.

Dynamics of Moscow SC footfall: Mall Index (weeks 1–48)

Footfall: Saint Petersburg

The attendance of St. Petersburg’s shopping centers has gone down by 0.3% for 11 months of 2024 versus a similar period last year. The footfall in Saint Petersburg’s shopping centers in Q4 2024 proved to be below the level of 2023 for a similar period by 4%. Taking fluctuations in the Index dynamics into account, this indicator has contracted by 0.3% versus last year for 11 months of 2024 and by 0.4% vs 2022. In our estimation, the footfall in SCs will be rebounding during 2025.

Dynamics of St. Petersburg SC footfall: Mall Index (weeks 1–48)

Source: the data of Focus Technologies, calculations of Nikoliers

Vacancy rate: Moscow and Saint Petersburg

|

6.4% |

Vacancy rate in Moscow’s shopping centers: Q4 2024 |

Based on the results for 2024, the vacancy rate has decreased by 0.5 p.p. versus Q3 2024 and by 3.6 p.p. versus the results for 2023. The highest vacancy rate of 15.5% can be found in neighborhood centers. In Moscow’s community centers the vacancy rate stood at 8.3%, in regional centers - at 4% and in superregional centers - at 3.8%. In our estimation, in three years to come the average vacancy rate will stabilize at the level of 6-7%, which will be caused by the commissioning of new small-sized facilities and the slowdown of expansion by Russian and foreign retailers, which will keep the market in balance.

|

3.1% |

Vacancy rate in St. Petersburg’s shopping centers: Q4 2024 |

The vacancy rate in St. Petersburg’s SCs kept sliding, having decreased by 0.3 p.p. versus the previous quarter. This can be explained by a high activity of retailers and the shortage of new retail premises.

The vacancy rate at the end of this year has contracted more than twice year-on-year, which became possible due to the lease of vacated spaces in IKEA malls by Megamarket marketplace (over 55,000 sq m) in the second quarter of 2024.

In spite of the fact that in 2025 five new retail facilities are slated for commissioning, the vacancy rate will increase insignificantly. According to our forecast, this indicator may reach 3.7% across the city, on the average.

Vacancy dynamics of retail space in shopping centers of Moscow and St. Petersburg

Source: Nikoliers

Online retail

According to Data Insight, in 2024 the volume of sales via the Internet will amount to RUB 10.1 trillion or 21% of total retail turnover in Russia. The market expansion has reached 28% this year. Online sales are expected to contract in three years to come due to the scale effect and will drop to 9% by 2027.

The E-Grocery market is rapidly expanding: during the year it has grown 1.5 times to RUB 1.1 trillion. It’s important for retailers to develop online sales in addition to offline channels. Modern-day consumers combine traditional visits to brick-and-mortar stores with shopping via mobile apps and websites.

The issues of regulating the activities of marketplaces are also being actively worked out, given that their share in E-Commerce turnover has already exceeded 80%. A respective bill will be submitted to the State Duma of the Russian Federation early next year. The document is aimed at creating more transparent and fair conditions for market participants, which may contribute to stiffer competition.

*As estimated by Nikoliers

Source: Rosstat, Data Insight, Nikoliers

Trends and forecast

Vacancy reaching plateau

Flagging development activity and dominance of small-sized facilities in the new construction have brought down the vacancy rate in shopping centers to its record low for the recent 10 years. According to our forecasts, in three years to come this indicator will stay consistently low, showing only minor fluctuations within 0.5 p.p. These changes will be associated with the entry of individual shopping centers of ‘regional’ and ‘super-regional’ scale to the market, expansion of Russian and foreign brands, as well as optimization of their already opened spaces.

Shopping centers as new spaces for recreation and communication

Modern shopping centers are transforming into life-style hubs, offering visitors not only shopping but also a variety of other opportunities. Such spaces are becoming a place where entertainment, culture and comfortable leisure blend harmoniously. For example, Okhta Mall (St. Petersburg) now allows visitors to bring their pets thanks to a pet-friendly policy, while MÖBELBURG has opened a co-working space and a lecture hall for creative folks. These initiatives bring shopping centers closer to the needs of their audiences, offering unique experiences and pushing the boundaries of their use.

Emotions instead of discounts: trending towards event marketing in SCs

Shopping centers seek to create unique experiences that cannot be replicated in the online space. For example, the Greenwich shopping mall hosted the Harry Potter Universe exhibition, immersing guests in the magical world through interactive rooms and masterclasses, while the VEER Mall installed a glass court for the Russian Squash Championship, allowing spectators to become part of the sporting event. This approach includes not only cultural and sporting events, but also non-standard campaigns, such as organizing an open training session for the Akhmat football club in Grozny Mall. Such initiatives help the shopping center stand out in the midst of competition and build up their footfall.

Anna Nikandrova, partner, regional director Retail and Property Management Department: "Modern shopping centers and stores are increasingly becoming multi-format facilities, combining different functions in one space. This meets changing needs and creates a unique experience for visitors. The given trend is exemplified by a growing share of shopping galleries in mixed-use developments (mixed-use centers or MUCs), transport and interchange or transfer hubs (TIHs) as well as in stylobates of residential projects. In 2025, the focus of developers will shift to such projects, which will let them attract a wider audience and create additional public spaces for recreation, work and shopping. However, the implementation of multi-format solutions requires significant efforts and goes beyond the traditional retail format. Low development activity and a shortage of quality space limit retailer expansion, whereas the growing key rate in the medium term will restrain deeper renovation or even re-conception of existing SCs. Under these circumstances, the efforts of professional management companies will allow developers to maximize returns on their projects and effectively adapt the space to changing market needs."