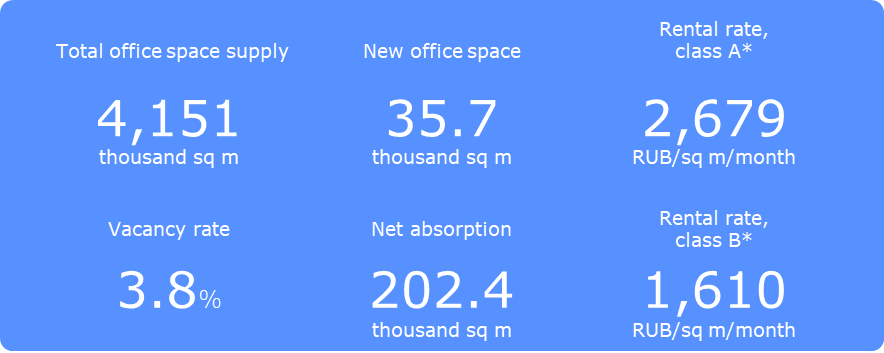

St. Petersburg market indicators, Q3 2024

Key results

Supply

For the nine months of 2024, the Saint Petersburg office estate market saw six new facilities added to it (total GLA is 35,700 sq m). Two of them were commissioned in the third quarter, namely Bogush Center and Avantgarde with the aggregate leasable area of 12,100 sq m.

Under the shortage of vacant space in existing buildings, demand for newly built facilities remains high. By the time of their commissioning lease agreements have already been signed to the office space available there. Thus, Avantgarde business centre is already occupied by a single tenant, whereas in Bogush Centre office development 12% of the office space is occupied and views never stop.

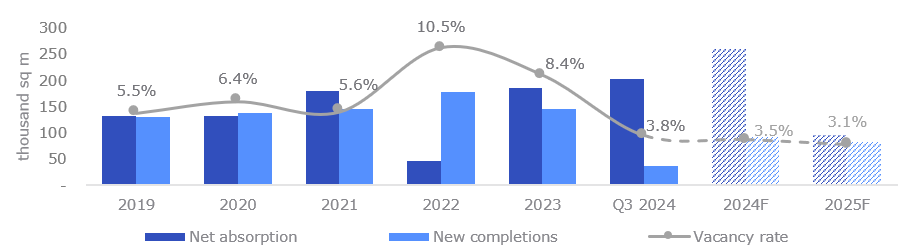

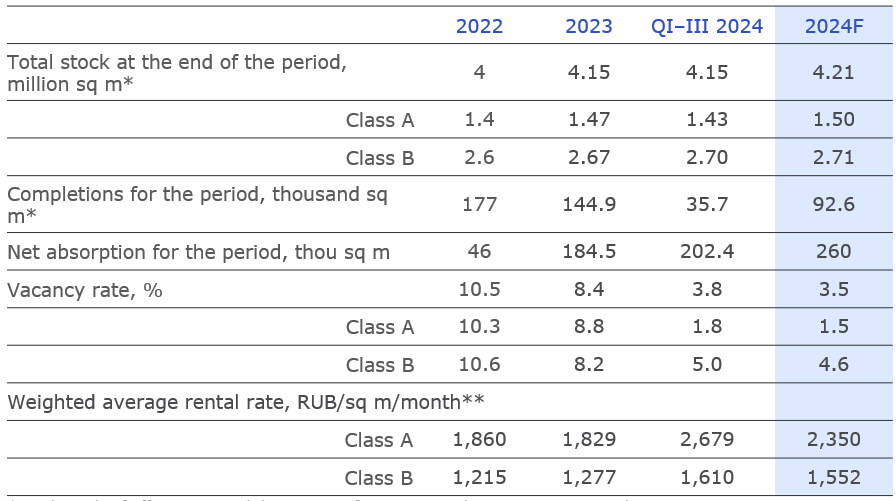

Dynamics of key market indicators

The forecast is the estimation of Nikoliers on the basis of announced delivery deadlines and data on the current status of projects.

*The rental rates are weighted average ones that do not include VAT. They are calculated with reference to vacant units offered for lease at the end of the period under review.

On account of methodological changes, the rental rates in the report have been reviewed with reference to vacant units across all periods, including the past ones, since prior to Q3 2024 calculations had taken into account the entire gross leasable area of all office buildings.

Source: Nikoliers

Vacancy rate and rental rates

|

3,7% |

Vacant space has shrunk more than two times relative to the end of 2023. |

|

|

A consistently high demand for quality office premises leads to a significant reduction of vacancy. In nine recent months vacant space has dropped from 8.4% (348,500 sq m) to 3.8% (159,800 sq m).

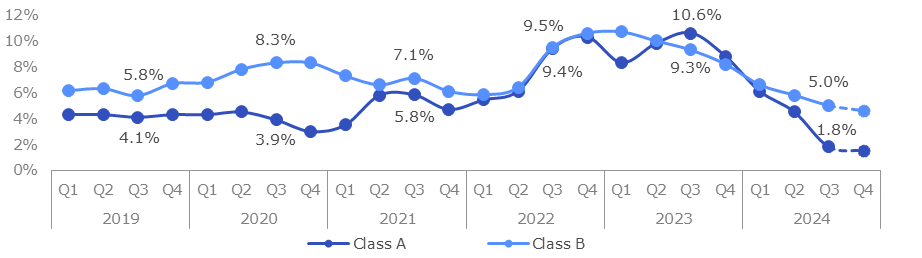

The vacancy rate in A-class offices has fallen by the record 7 p.p. since the end of 2023 (from 8.8% to 1.8%). The absorption of large units and the lack of new construction on A-class offices in recent nine months notably limit the choice of suitable space for demanding occupiers seeking the high quality of office space. Till the year’s end the commissioning of a single A-class facility is expected, but it has already been occupied, and so the scarcity of supply won’t go anywhere. Highest quality offers in class B, which are not inferior to class A in terms of location and infrastructure, will keep being contracted and occupied as well.

Vacancy rate by class

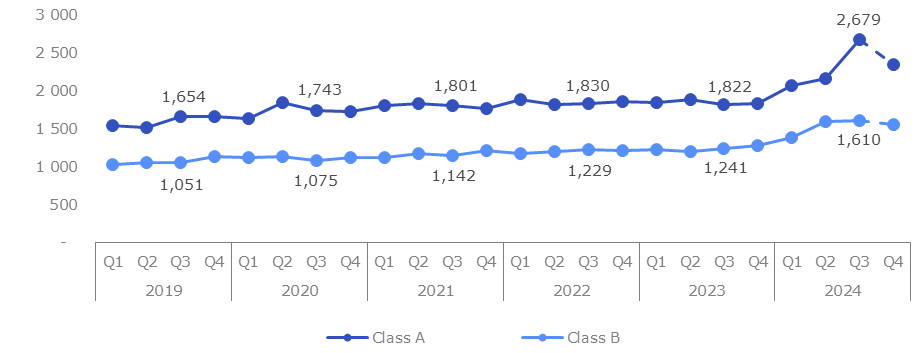

Given the acute shortage of supply in class A, the weighted average rental rate for such premises has gone up 46% since the turn of the year. Mainly smaller units from 150 to 800 sq m are left on the market, whereas larger ones from 1,000 sq m have been occupied. There are large-sized vacant premises in B-class office centres, including entire floor levels, in high-quality B-class business centres. Under the short supply on the market, such offers are comparable in terms of the rental rates to A-class offices.

In view of the limited supply, the rental rates are highly volatile; therefore, as liquid options are absorbed, we can expect stabilization of the rental rates towards the year’s end for the supply in exposure at the level of RUB 2,350 per sq m per month in class A and RUB 1,550 per sq m per month in class B, but the amount of office space for lease will further shrink drastically. Thus, the growth of the average market rental rate may reach 15% at the end of the year.

Change in rental rates by class*

*The rental rates are weighted average - they include OPEX but exclude VAT, being calculated with reference to vacant units offered for lease at the end of the period under review..

Source: Nikoliers

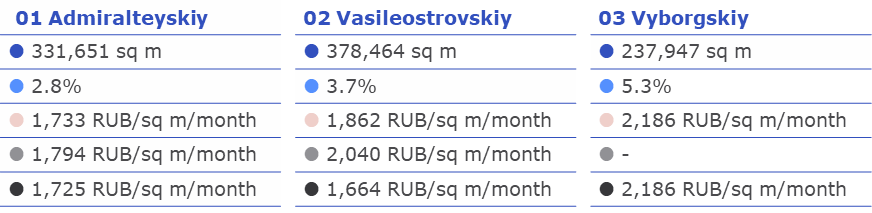

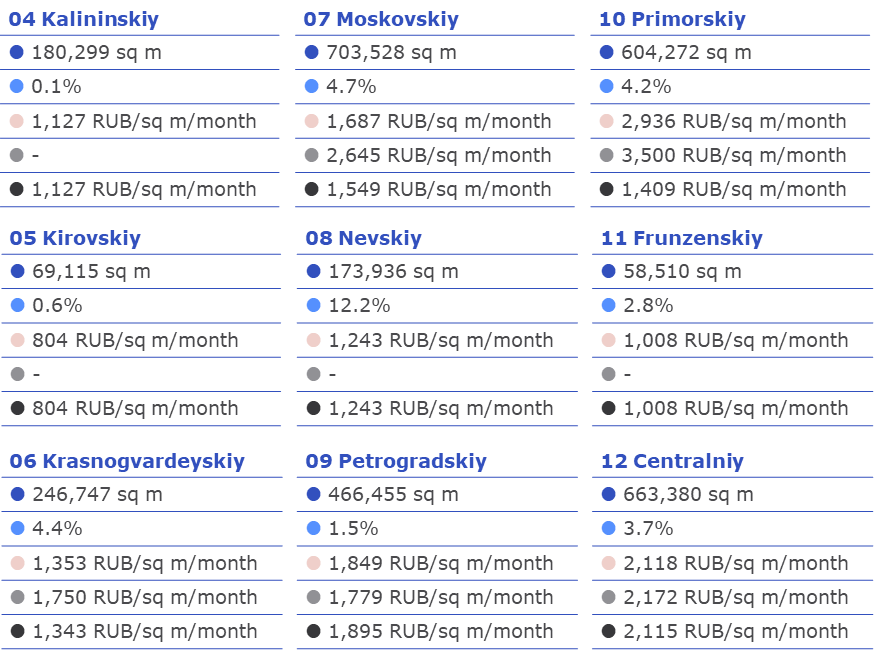

Key market indicators by districts*

Source: Nikoliers

*The rental rates quoted are weighted average ones; they include OPEX but exclude VAT. They are calculated with reference to vacant units offered for lease at the end of the period under review.

Demand

|

31% |

The IT&T segment is still the leader in terms of total occupied office space after 9 months of 2024. |

The demand for quality office premises remains high. The net absorption almost six times exceeds the amount of newly built office space.

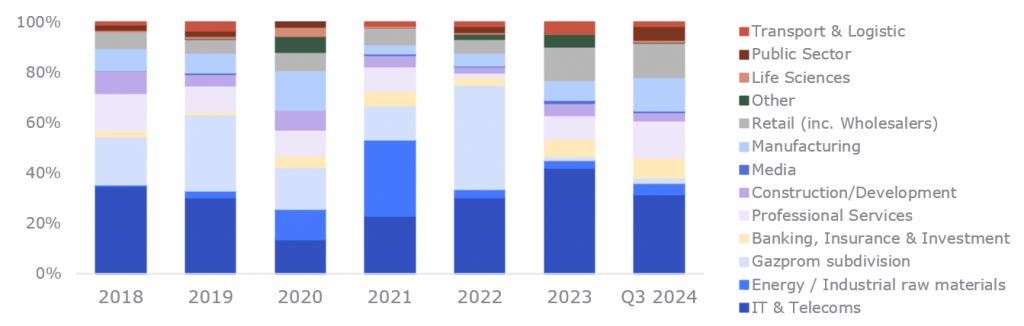

Companies are highly interested in the lease of entire floor levels or even entire office buildings. More than a third of transactions in class A and 20% of transactions in class B were made with premises in excess of 1,000 sq m.

In 2024 the demand for offices larger than 5,000 sq m has grown by 5.5 times as compared to the year before. Banks and IT companies preferred large offices in quarters I-III of 2024. Due to the demand for large office space, the number of transactions with manufacturing companies providing professional services has tripled. The number of transactions concluded by retail companies has also doubled due to the purchase of Space BC by Petrovich.

Distribution of deals by tenant type

|

202.4 |

Net absorption for the nine months of 2024 was 10% higher than the final figure for 2023. |

|

thousand sq m |

Trends and forecast

Key market indicators

*Total supply of office space and the amount of commissioned space were corrected in Q3 2024.

** The rental rates are weighted average and include OPEX but exclude VAT; they are calculated with reference to vacant units offered for lease at the end of the period under review.

Acute shortage of А-class office premises

The lack of new construction projects at scale and vibrant demand for A-class offices have resulted in considerable contraction of vacant space. Almost no vacant units are left in this segment on the Saint Petersburg office estate market, and this situation will remain unchanged till the year’s end.

Tenants looking for alternatives

In the midst of acute shortage in Class A and rapid absorption of top-quality offers in Class B occupiers are willing to consider offbeat solutions. Under the stiffening competition for office lots, interested occupiers are ready to wait for office space that may potentially be vacated, exploring alternative options of accommodation in serviced offices or leasing office space in off-plan projects.

High absorption rates

Occupiers are still interested in quality offices and so a high level of absorption is expected as the main result of this year. The scarcity of office space is a major contraint on the faster growth of transaction numbers; however in the newly built office space to be commissioned till the year’s end only 15% of office space is currently vacant.

The fast absorption of liquid lots will lead to the reduction of estimated rents due to changes in the supply structure, while the price of vacant spaces will soar high.