*Weighted average rental rates do not include operating expenditures (OPEX), utility payments and VAT (20%). Calculated on the basis of vacant supply in existing projects inside the Moscow Ring Road (MKAD)

Main results

.png")

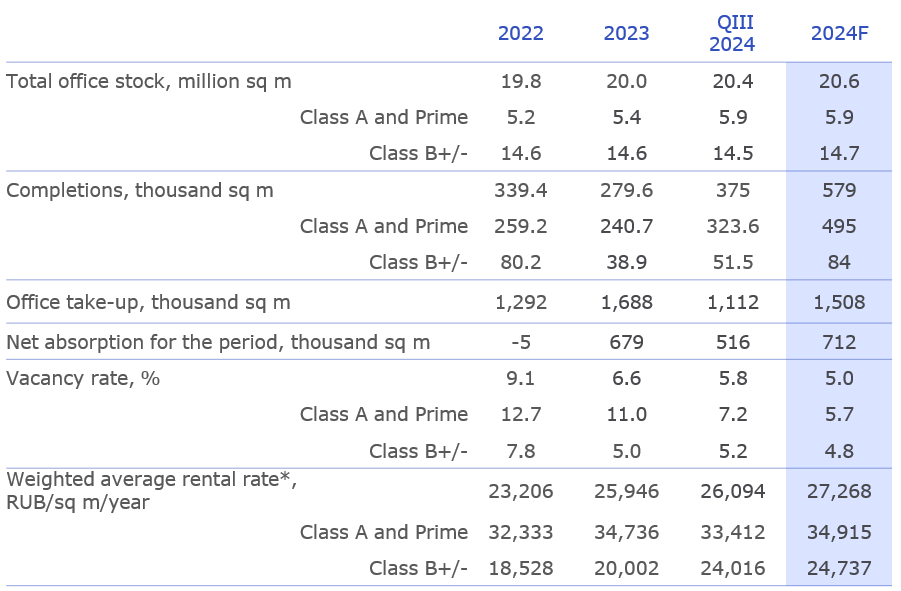

Key market indicators

Forecast - as estimated by Nikoliers based on the announced commissioning deadlines and data on the current status of projects.

Source: Nikoliers

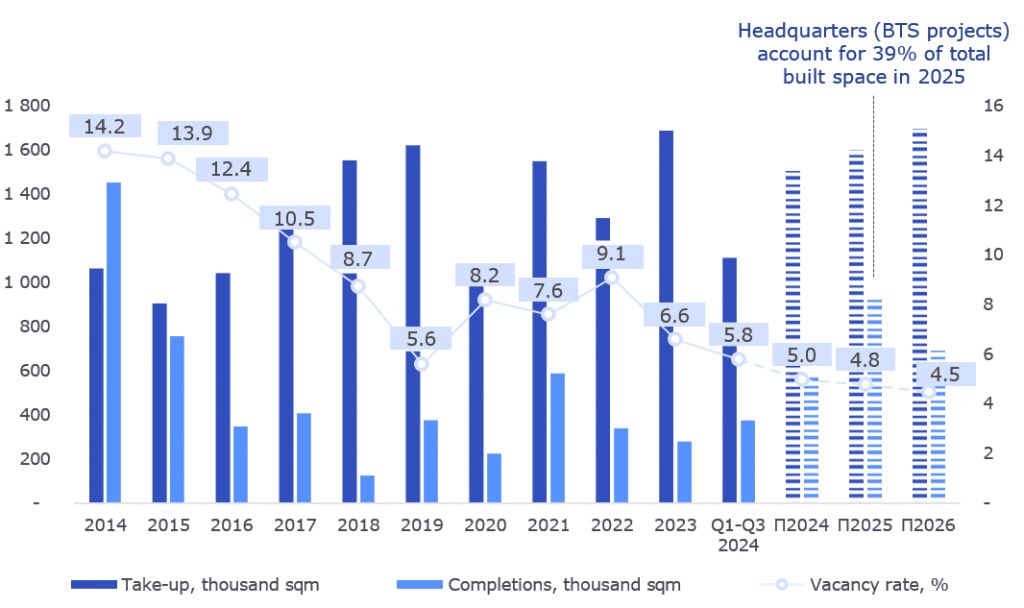

Supply

Office completions, QIII 2024

For the initial nine months of 2024, 375,000 sq m of office space have been completionsin, of which 81% are already under pre-lease and pre-sale agreements and almost 2% falls to the share of build-to-suit space (GBU Mosgorgeotrest). Overall, 66,000 sq m are available, of which 78% is located between TRR and MKAD, while 22% is outside the MKAD. On offer for lease is only limited office space outside the TRR in the north of Moscow (6,000 sq m) and in Skolkovo (14,000 sq m), the rest office space being put on sale.

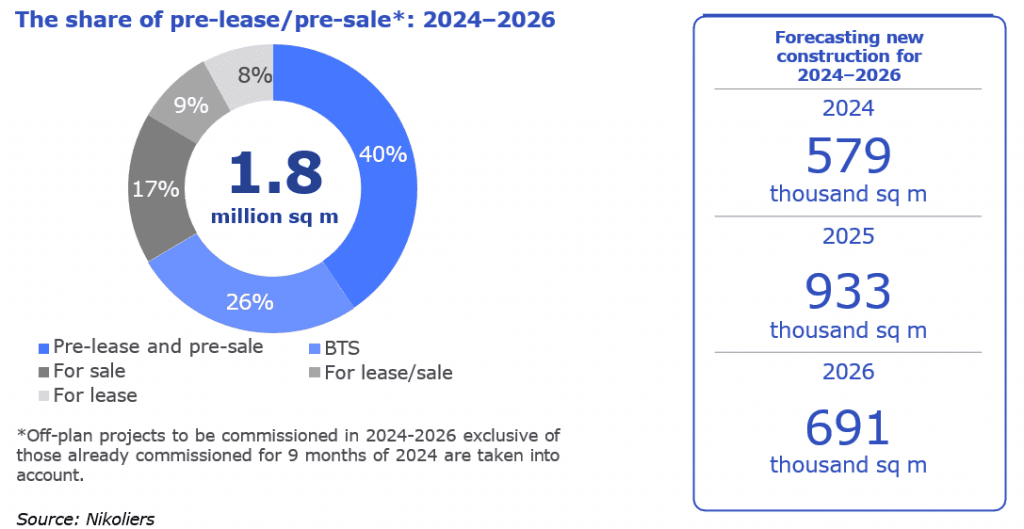

Nikoliers predicts that till the end of 2026, another 2.8 million sq m of office space will have been commissioned, with only 240,000 sq m available for lease. This limited amount of built space for lease in the midst of high demand for large units further aggravates the scarcity of rental supply in the Moscow office space market.

Dynamics of office space commissioning, thousand sq m

.png")

Forecast - as estimated by Nikoliers, based on the announced commissioning deadlines and current status of office projects.

Source: Nikoliers

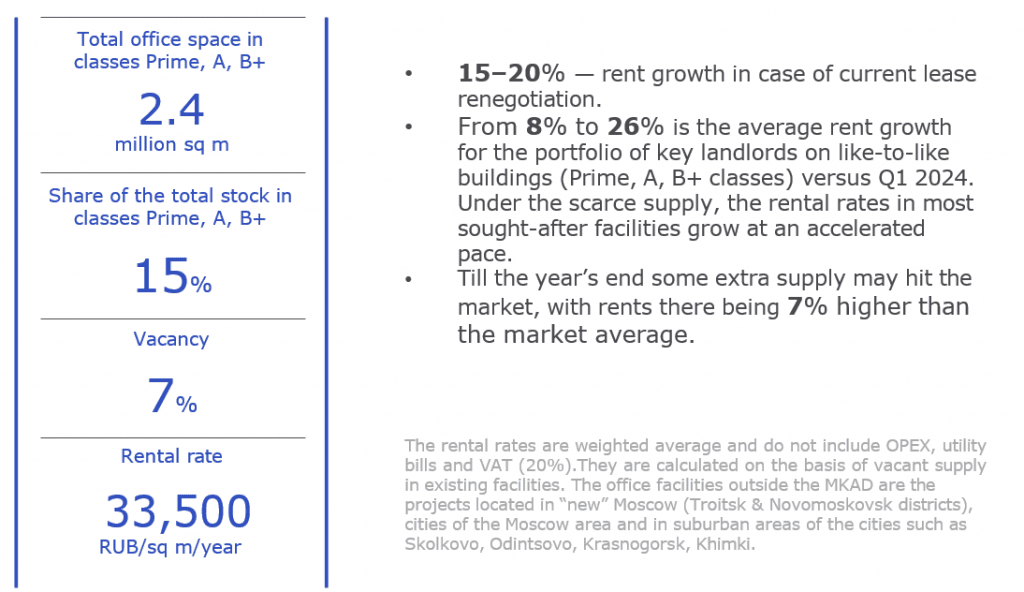

Commercial terms

4.5 % Growth of the average rental rate for nine months

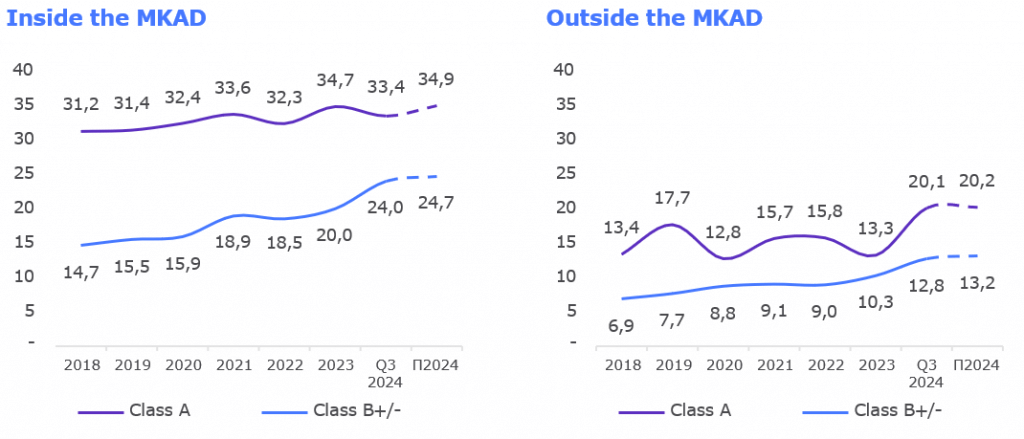

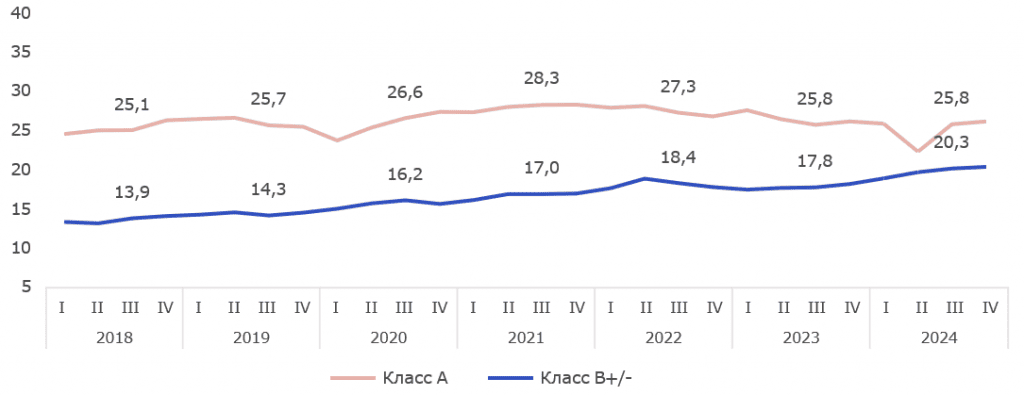

The rolling of costly supply outside the MKAD out to the market is a factor of growth for average market indices. Earlier in locations remote from the centre, the rental rates were way lower than the market average and the amount of vacant space was pulling the rental rates down. The commissioning of a new high-quality project pushes the estimated rent up. For nearly seven years the average market rental rate inside the MKAD on vacant supply in exposure has increased by 30%, while outside the MKAD it rose by 77%.

Dynamics of rental rates by location, classes, thousand RUB/sq m/year

The portfolio of 13 key owners

Commercial terms

Several factors contributed to rent growth, based on the results for three quarters of 2024. First of all, units in quality buildings, offered at the rates above the market average, hit the market. Furthermore, the owners of projects in highest demand raise the rental rates amid the acute scarcity of such office space. The rent for such units in classes A and Prime surged from 7% to 29% per quarter.

Under a shortage of quality units, the choice of office space in classes A and Prime is limited, with B-class facilities prevailing. The rental price of the latter also keeps growing, since they are a good alternative to occupiers contemplating large units from 3,000 sq m and larger.

Dynamics of rental rates* by classes, thousand RUB/sq m/year

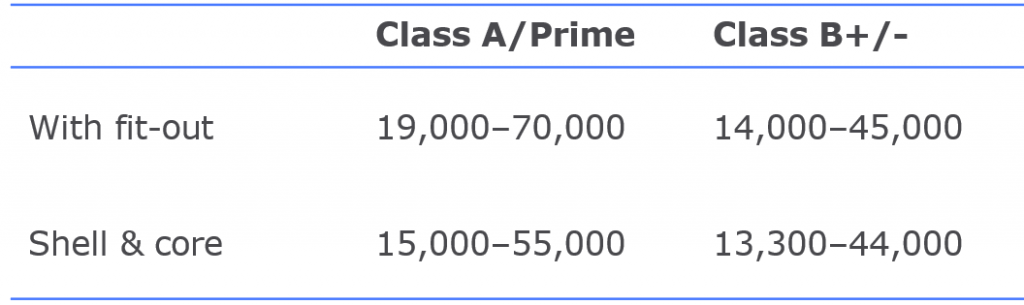

In classes A and Prime, the estimated weighted average rental rates for premises with and without fit-out have almost aligned. Given the limited vacant supply in central Moscow, the few large office units in excess of 10,000 sq m available are offered in the high pricing range. These are one-off cases, whereas the average rental rate for shell-and-core A-class office premises, exclusive of outlying figures, stand at about RUB 30,000 per sq m per year.

Offers with fit-out may vary widely in terms of quality: from top-quality premium finishes to office premises with a standard fit-out. As for office premises with fit-out, the average rental rate amounted to RUB 40,000 per sq m per year, up 12% versus Q1 2024.

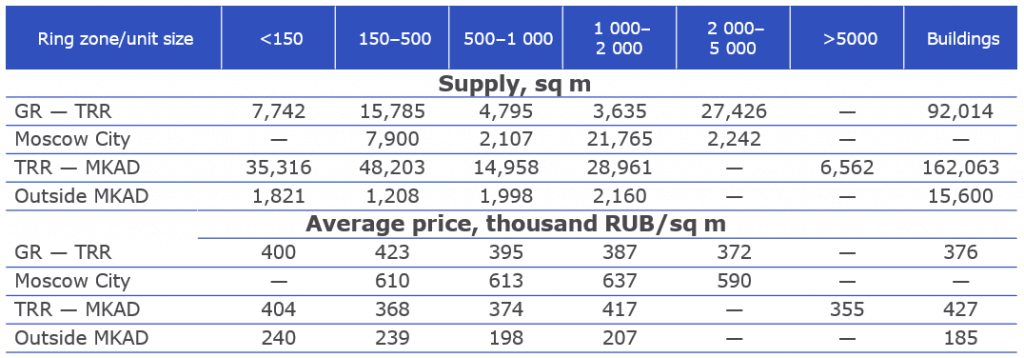

Rental rates by types of premises, classes, RUB/sq m/year

The rental rates are weighted average; they and do not include OPEX, utility bills and VAT (20%), calculated by vacant supply in existing facilities. The office facilities outside the MKAD are the projects located in “new” Moscow (Troitsk & Novomoskovsk districts), cities of the Moscow area and in suburban areas of the cities such as Skolkovo, Odintsovo, Krasnogorsk, Khimki.

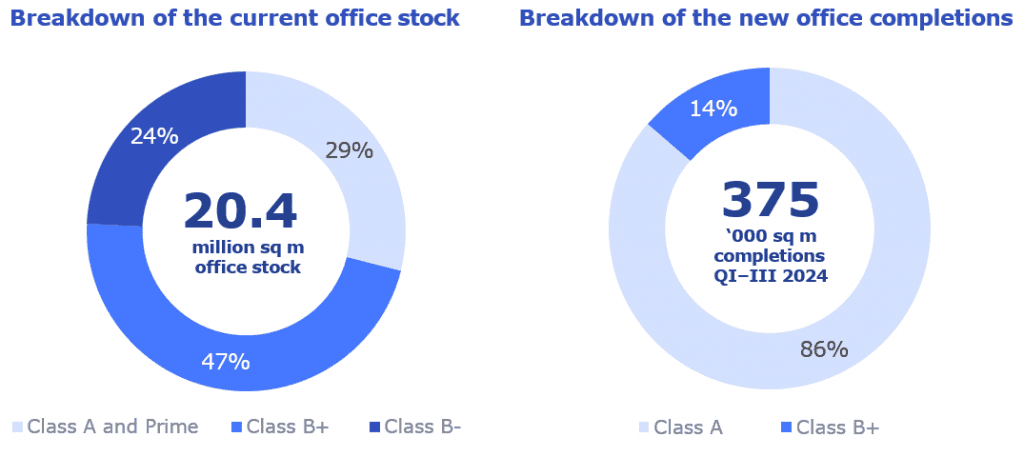

Breakdown of office vacancy in off-plan projects

The acute scarcity of supply in the office estate market upholds the demand for the lease and purchase of offices in buildings under construction. This is why by the time of construction completion some 70-90% of the available new office space is already contracted. Overall, 375,000 sq m of office space have been commissioned with only 18% of this space being vacant. We’ll see this trend continued in two years to come. The average vacancy rate in off-plan projects to be commissioned in 2024-2025 is at the level of 34%.

Vacancy dynamics in completed projects

- 0.8 p.p Reduction of average market vacancy for nine months

Vibrant absorption of office space in existing buildings and low vacancy in the already commissioned facilities are conducive to a persistently low amount of vacant space. The upward correction of vacancy in class A has to do with the vacation of several large units. The exposure of this offer won’t be long, since the structures of biggest companies will quickly occupy the top-quality options.

Vacanct space share by classes

Source: Nikoliers

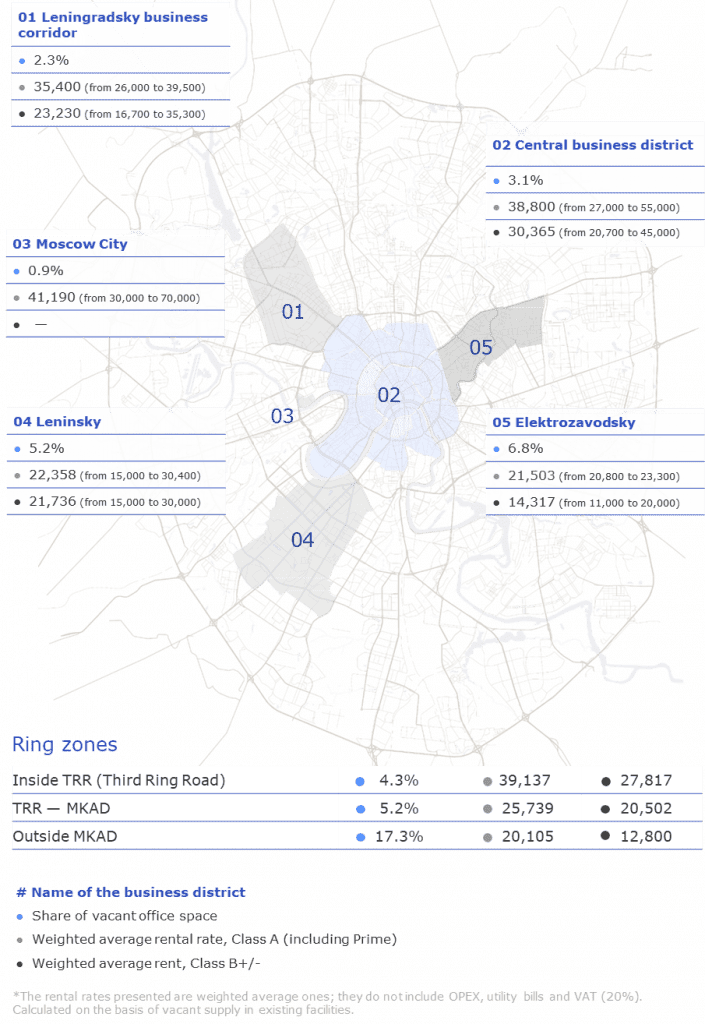

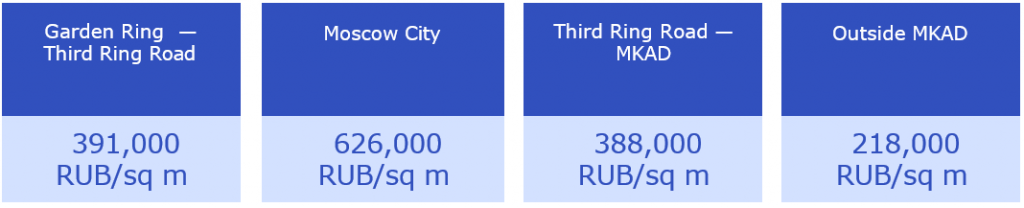

Key market indicators by business districts*

Office space offered for sale in the in projects under construction

Weighted average cost of office units in buildings under construction

The purchase of off-plan office space is still in demand. Investors are attracted by the potential of such transactions amid the anticipation of growing prices and flexible payment terms offered by some developers against the high cost of debt financing.

The demand for office space from end users is conditioned on the needs of growing business at scale, as well as by the shortage of office space for lease and the prevalence of options for sale in exposure.

Both for investors and end users investing in the office purchase today is the opportunity to hedge their capital in long-term planning.

Off-plan office space supply at the stage of construction

The cost shown on this page includes VAT with the exception of projects delivered on the basis of shared- equity agreements.

Hereinafter: Moscow areas outside the MKAD, including but not limited to Troitsk and Novomoskovsk districts, cities of the Moscow Region as well as suburban areas of the cities Skolkovo, Odintsovo, Krasnogorsk, Khimki.

Source: Nikoliers

Office take-up

Total transactions for QI-III 2024

At present, demand is curbed by the shortage of supply that would meet the needs of companies. Some of this need can be satisfied by way of office space purchase instead of lease and offbeat settlement solutions which certain landlords have to offer. Yet such options do not always allow the immediate move-in, which creates the effect of accumulated pent-up demand.

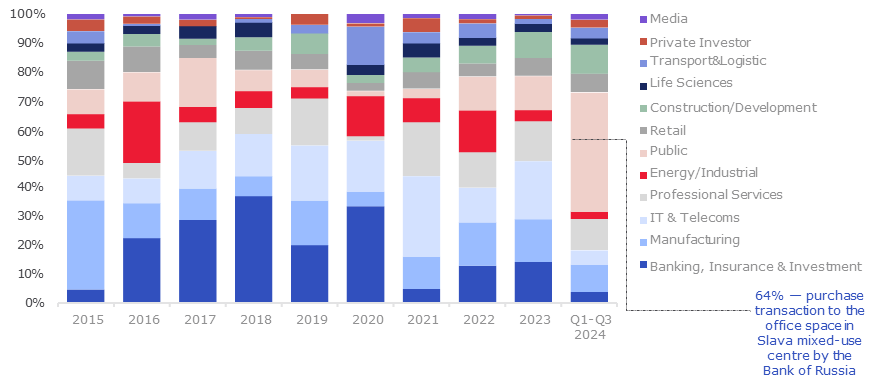

Breakdown of demand by business sectors of companies

Key business sectors by the amount of demand for 9 months of 2024

Key lease transactions in the Moscow office market for 9 months of 2024

.png")

*The demand takes into account transactions in the off-plan market, but does not include investment purchase-sale contracts for completed projects with an existing rental flow.

Source: Nikoliers

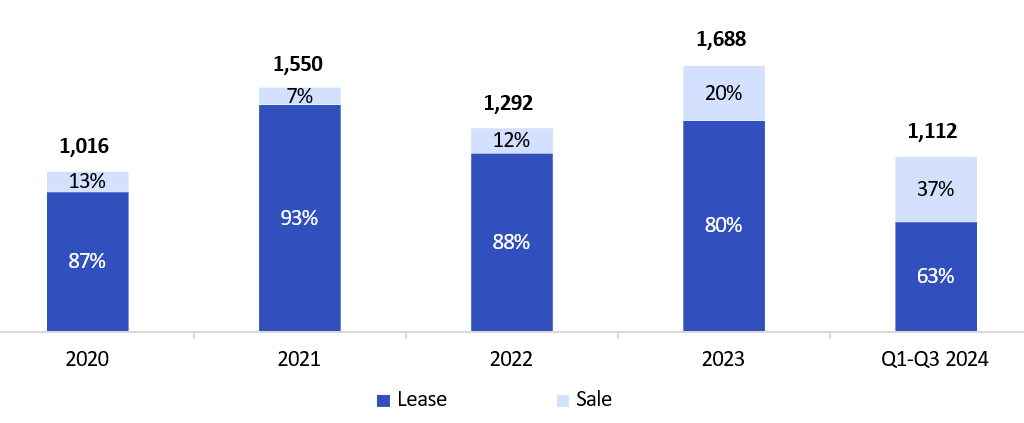

Breakdown of demandThe amount of office space lease and sale, thousand sq m

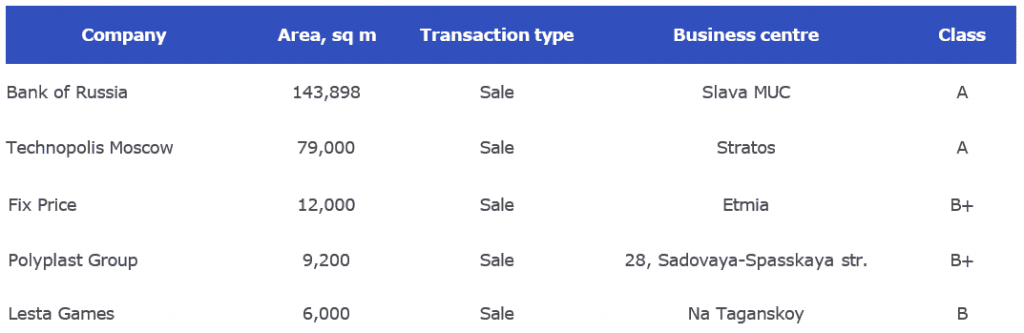

A high share of purchase and sale transactions is related to persistently high interest in the purchase of office space and limited lease offers in exposure. The purchase of 144,000 sq m in Slava MUC by the Bank of Russia accounted for 13% of total demand and 35% of bought space. This is the largest transaction of acquiring a building by the end user in the office market of Moscow. Government agencies have been keen on the office market since 2023.

Key sale deals in the office market of Moscow for 9 months of 2024

Source: Nikoliers

Key market indicators and forecast

*The weighted average rental rates do not include OPEX, utility bills and VAT (20%), and are calculated with reference to vacant supply in existing facilities inside the MKAD.

Office market trends and outlook

Demand for office space exceeds supply

The shortage of quality supply and the lack of newly built office space for lease lead to the situation, where the demand for offices is higher, than the available supply. With that said, seekers after office space demonstrated their willingness to wait for the vacation of attractive office units not to miss on the opportunity to occupy them. According to our forecast, high office space absorption rates will persist.

The burgeoning share of sold office space

The shortage on the office lease market will spark interest in the aquisition of buildings in the overseeable future. For all that, the interest in purshases is expected from the companies that did not care about this option before, but later accumulated the pent-up demand as they kept waiting for suitable alternatives.

Growing rents not only to vacant units

Under the current circumstances the rental rates will be appreciated not only on currently vacant options - commercial terms will be revised on units with expiring long-term lease agreements as well.The average growth on projects in highest demand may reach 15-20% per annum.

The total supply may change due to reclassification of the office stock, conducted by MRF.