MACROECONOMIC SITUATION

A high level of the key rate largely determines the dynamics on the national real estate market, including in the industrial segment. An increase in the cost of debt capital lowers the activity of developers and investors, limiting their possibility to finance new projects and to upgrade the existing ones.

The given situation slows down the pace of construction on new warehouses and cripples the refurbishment of old facilities. Developers are forced to revise their plans and to optimize their budgets, often sacrificing the technical characteristics or scale of their projects, chasing economic expediency. Furthermore, the high key rate makes short-term loans, needed to finance the current operating expenditures and to upkeep the stable business operation, more expensive and less attractive.

According to a macroeconomic survey conducted by the Bank of Russia, relatively high values of the key rate will be preserved in the near future, which will increase the negative impact upon the industrial real estate sector. Without effective measures to boost investment activity and lower the cost of debt financing, recovering the balance between demand and supply in the industrial real estate market may prove to be a long and complicated process.

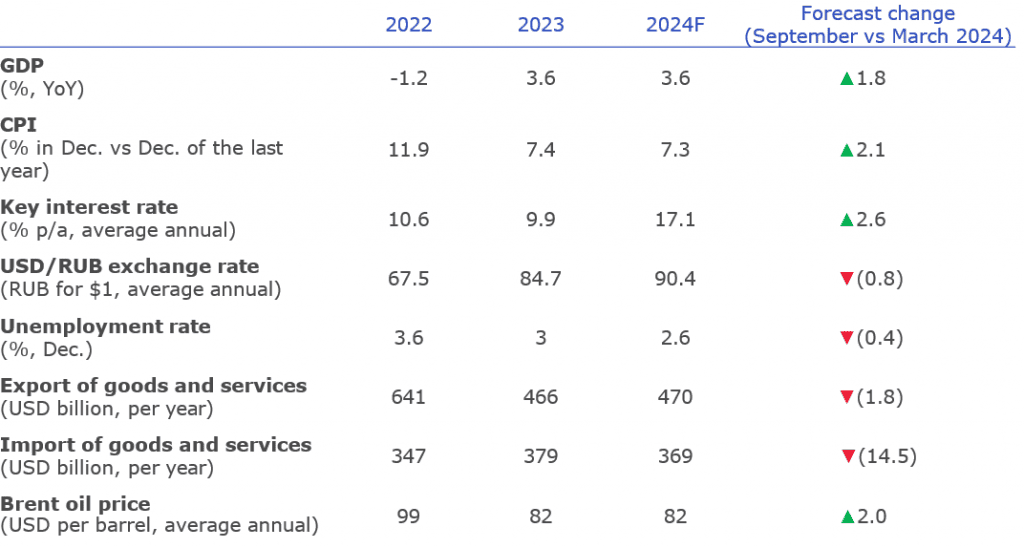

Key macroeconomic indicators of the market

Source: Macroeconomic survey conducted by the Bank of Russia as of September 2024

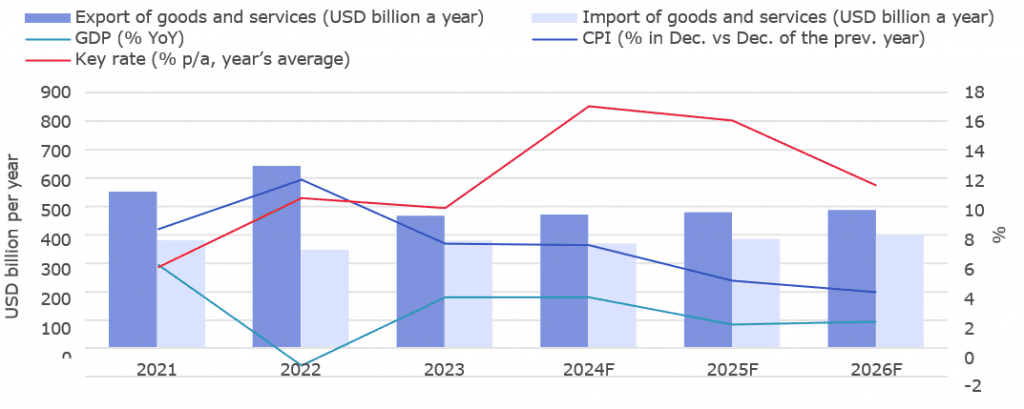

Dynamics of macroeconomic indicators in Russia

Source: Macroeconomic survey conducted by the Bank of Russia in September 2024

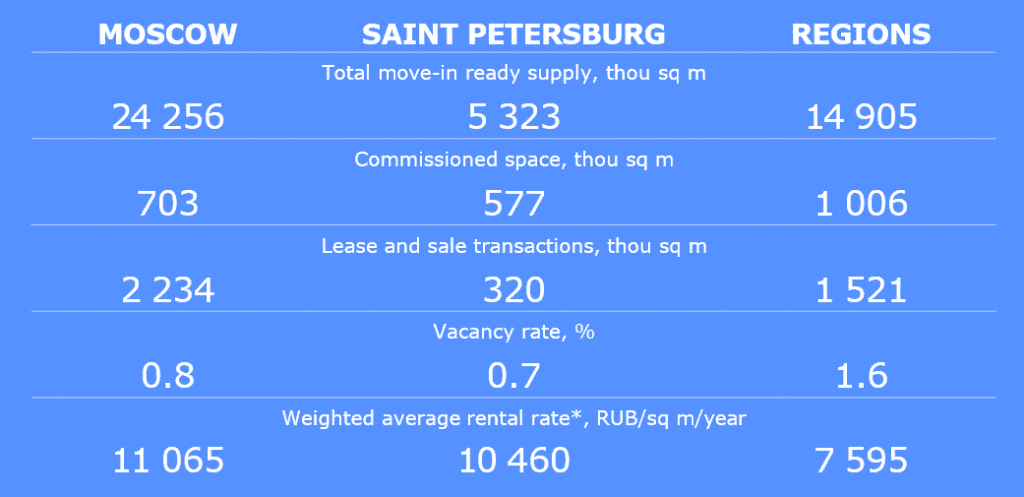

KEY MARKET INDICATORS, Q3 2024 (CLASSES А and В)

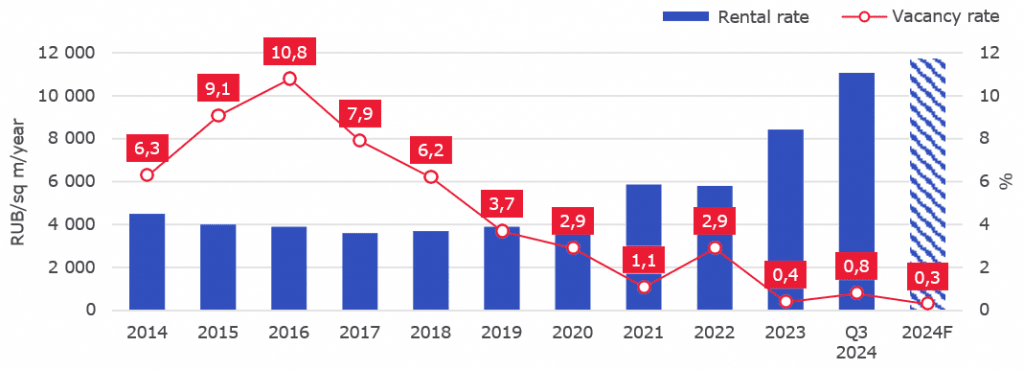

The industrial real estate market in Russia continues to demonstrate rent growth and acute shortage of vacant space. Thus, the weighted average base rent in Moscow has already exceeded RUB 11,000/sq m/year.

The tightening of the macroeconomic situation in the country makes the construction of storage facilities a more complicated process. Thus, some of the warehouse projects, originally scheduled for commissioning this year, have been pushed back to 2025. Yet the anticipated aggregate new supply will stay at a record level this year - 5.3 million sq m.

Lease and sale transactions concluded on the market for the initial nine months of the current year total to 4.1 million sq m, which almost repeats the record level of the previous year. The given fact highlights robust activity and demand from various sectors of national economy for up-to-date warehouses.

Dynamics of key market indicators (nationwide results)

(1).png")

Source: Nikoliers

NEW SUPPLY

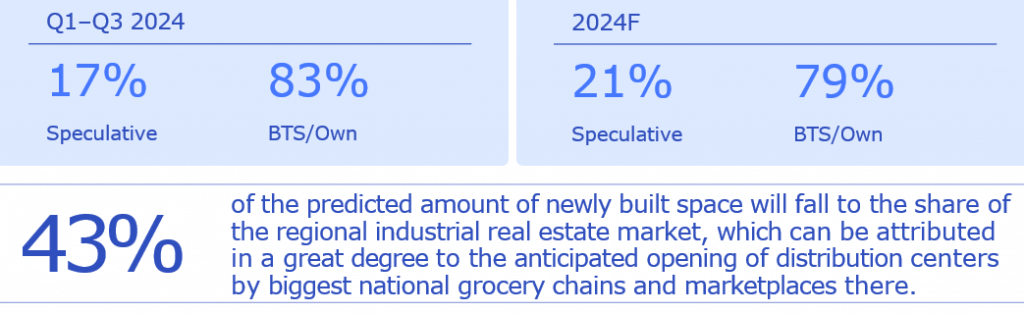

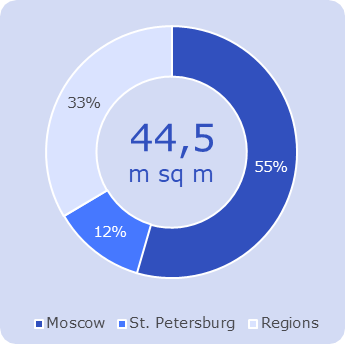

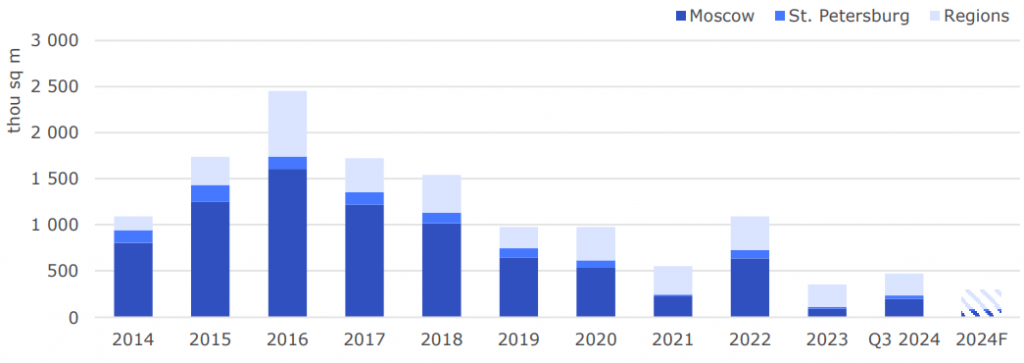

More than 2.3 million sq m of quality warehouse premises were commissioned for nine months of 2024 in the Moscow area, Saint Petersburg and Leningrad region as well as in other regions of Russia, the latter accounting for a prevalent share of these (44%). If we look more closely at the newly commissioned space, half of it (52%) was turnkey facilities.

Expected for commissioning in Q4 are about 3 million sq m and so the cumulative new supply may potentially reach the record 5.3 million sq m. Yet this robust development won’t be a turning point for the market. The shortage of vacant supply will persist because the given result is largely the consequence of major build-to-suit transactions concluded in the past years.

Commissioning dynamics in key markets of Russia

.png")

Commissioning dynamics by type of construction, thou sq m

Source: Nikoliers

A high level of the key interest rate and growing construction costs slow down the development of warehouse projects, especially specualtive ones, in view of higher risks on account of both the macroeconomic situation and market terms.

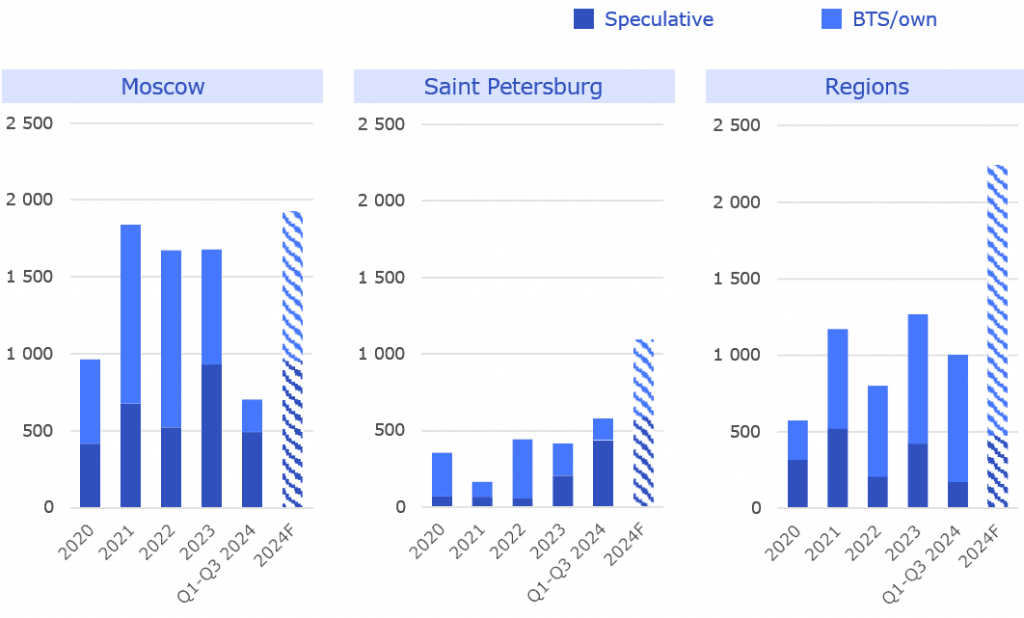

NEW SUPPLY: Moscow and Moscow Region

In Q3 2024, the supply of quality warehouses in the Moscow area increased by 293,000 sq m, of which 36% can be found in the Ozon distribution centre at PNK Park Domodedovo-2 industrial park. Overall, 703,000 sq m of storage space has been commissioned in the capital city this year.

All in all, the commissioning is predicted at the level of 1,928,000 sq m for 2024. At the end of the year the cumulative quality move-in ready supply may crack the 25-million-sqm mark.

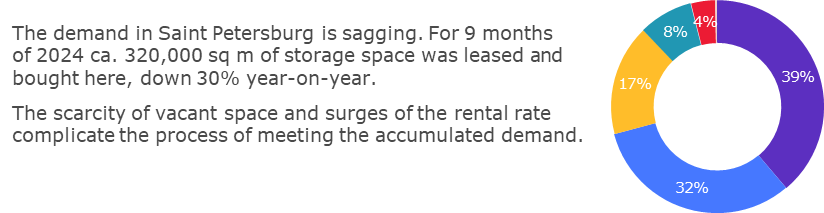

NEW SUPPLY: Saint Petersburg and Leningrad Region

In Q3 2024, the maximum quarterly commissioning was recorded in the industrial real estate market of the Russian northern capital: 394,000 sq m, which exceeds the previous peak, reached in Q4 2022, by 5%. The given result comes from the commissioning of some major industrial facilities, such as warehouse clusters 100K and Osinovaya Roscha (Aspen Grove) as well as a building in the industrial park PNK Park Kolpino.

A record commissioning of industrial space is anticipated for 2024: 1,095,000 sq m of which 53% falls to the share of speculative projects that were actually fully contracted already at the stage of construction.

Source: Nikoliers

NEW SUPPLY: Russian Regions

The regional market, where about 1 million sq m of storage space were commissioned, accounts for the largest amount of new quality supply across Russia for the three quarters of 2024.

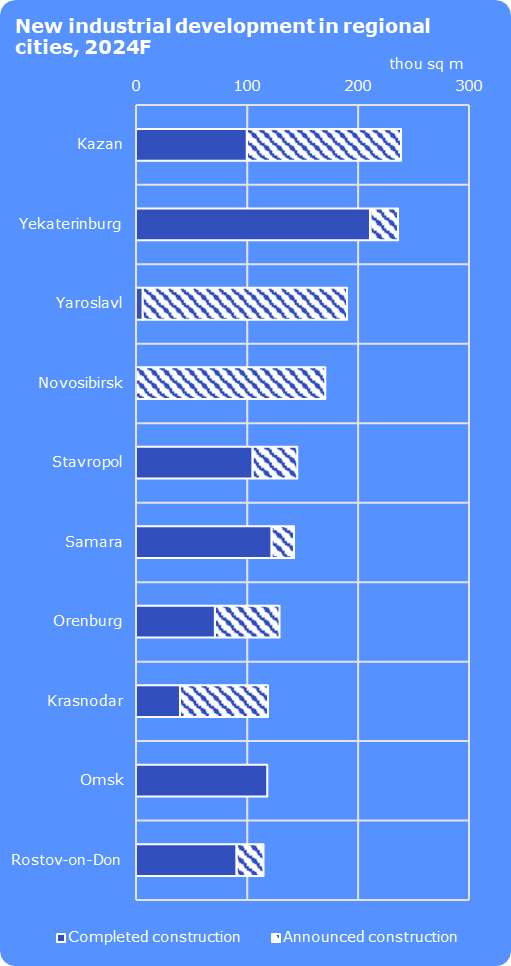

At the present moment the leading cities by the amount of commissioned industrial space are: Yekaterinburg (211,000 sq m), Samara (122,000 sq m), Omsk (118,000 sq m) and Stavropol (105,000 sq m). In total, the above- listed cities represent 55% of total new supply for the first to third quarters of 2024 on the market of Russian regions.

In Q4 2024 the largest commissioning is predicted in the following cities: Yaroslavl (183,000 sq m), Novosibirsk (170,000 sq m) and Kazan (134,000 sq m).

Overall for 2024, the industrial space commissioning in the regional market is predicted at the level of 2.2 million sq m. Thus, by the year’s end total quality supply of warehouses across the country may hit the mark of 47 million sq m by the end of this year.

Breakdown of move-in ready supply, Q3 2024

Source: Nikoliers

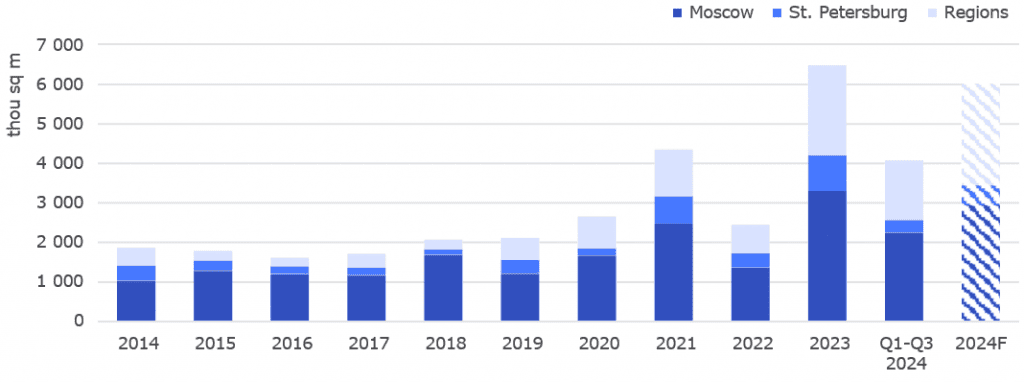

INDUSTRIAL SPACE LEASE AND SALE TRANSACTIONS

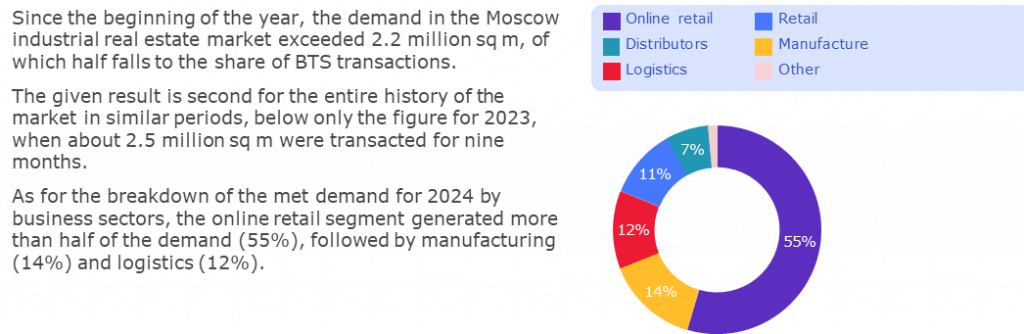

Today the industrial real estate market is among the fastest growing and most sought-after commercial real estate sectors in Russia. This is to a large extent a consequence of aggressive expansion and activity demonstrated by online retail companies which, given

a high demand for warehouse premises on their part, exert significant influence on construction volumes and business strategies of other market players.

Based on the results for the initial three quarters of this year, lease and sale transactions totaled to more than 4.1 million sq m, thereby actually repeating the record achievement of the previous year (4.2 million sq m). The short supply of quality vacant space across almost all markets leads to a growing number of build-to-suit transactions (56% of the total met demand since the beginning of the year)

Business activity does not abate. The sold and let industrial space during the first to third quarters is at the level close to record figures for the same period of the previous year.

Dynamics of concluded lease and sale transactions in key markets of Russia

Breakdown of concluded lease and sale transactions by type

Source: Nikoliers

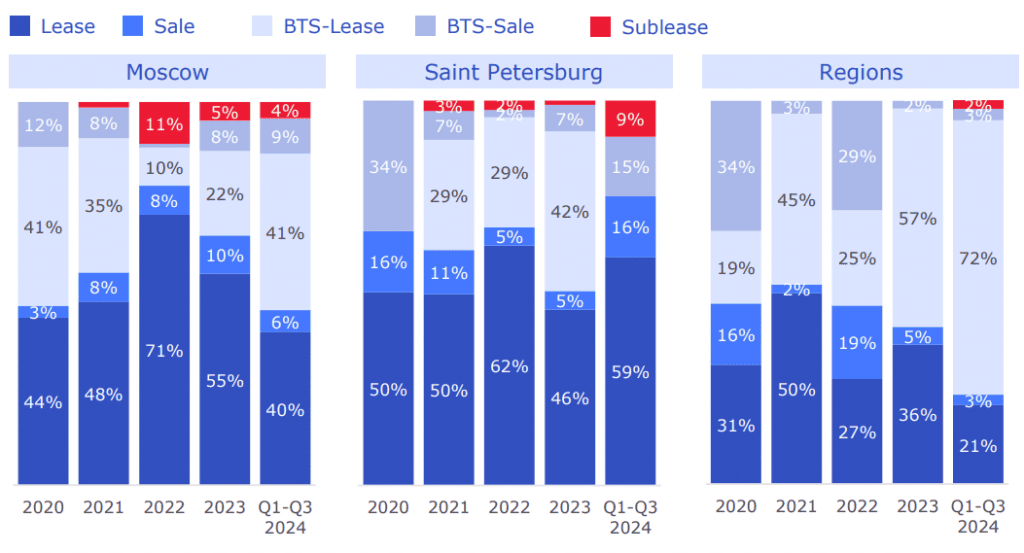

Concluded lease and sale transactions: Moscow and Moscow Region

Concluded lease and sale transactions: Saint Petersburg and Leningrad Region

Concluded lease and sale transactions: Russian Regions

Source: Nikoliers

VACANCY AND RENTAL RATES

At the end of Q3 2024, the total quality vacant storage space amounted to 470,000 sq m, which is equivalent to 1.1% of the total move-in ready supply in Russia. An insignificant increase in vacancy was caused by tenant rotation as well as the rollout of offers found in relatively old and lower quality facilities.

The current economic and market demand and supply ratio bolster further growth of rental rates in the Russian industrial real estate market: the persistent imbalance of demand and supply strengthens the positions of industrial landlords who keep raising the rent on account of hectic demand as well as growing OPEX and construction costs.

Vacant space dynamics in Russia’s key markets

.png")

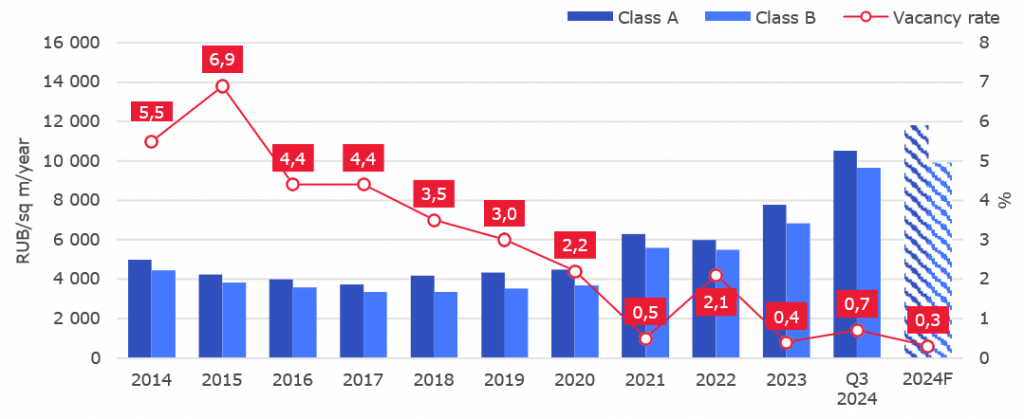

VACANCY AND RENTAL RATES: Moscow and Moscow Region

At the end of Q3 2024, the weighted average base rent for move-in ready warehouse premises in the industrial real estate market of the Moscow area stood at RUB 11,065 per sq m per year, up 7.2% vs. the previous quarter.

Dynamics of weighted average rental rate* and shares of vacant space

*The weighted average rental rate for move-in ready vacant dry warehouse premises is indicated, excluding OPEX and VAT

Source: Nikoliers

The vacancy rate in the capital city grew by 0.4 p.p. versus the end of the previous year reaching 0.8%. In absolute terms it’s 194,000 sq m. This slight increase will not be able to address the shortage of vacant industrial space on the market.

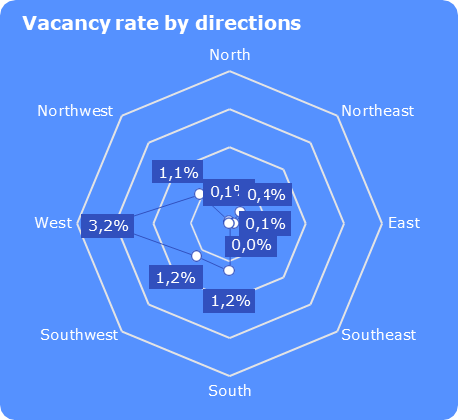

The most acute scarcity of vacant space can be felt along the eastern routes of the Moscow area, where the vacancy rate varies between 0.0% and 0.4%.

An increase in the vacancy rate along the western route was caused by the vacation of much storage space in a Class A warehouse complex located at a rather large distance from the Moscow Ring Road (MKAD).

The limited supply of vacant space and the shortage of large-sized units have sparked interest in high-quality premises currently under construction, where the rental rate is 10% higher compared to the earlier commissioned A-class facilities, already exceeding RUB 12,000 per sq m per year.

|

31% |

was the growth of the weighted average base rent for move-in ready warehouse premises of classes A and B in the Moscow area versus the end of 2023. |

If the change in the base rent is analyzed depending on the remoteness of warehouses from the MKAD, then within 10 km off the MKAD the weighted average rental rate for A-class warehouse premises may reach RUB 19,000 per sq m per year (triple net), which is higher than the average rental rate for A-class office premises outside the MKAD.

Traditionally, the distance from the MKAD and the rental rate are in inverse proportion to each other. Nevertheless, even at a distance in excess of 60 km off the MKAD the rental rate is higher than in 2023, when the weighted average figure stood at RUB 8,425 per sq m per year.

Breakdown of the weighted average base rent* by classes and distance from the MKAD (the circle size reflects the size of a vacant unit)

(1).png")

*The weighted average rent for move-in ready vacant dry warehouse premises (classes A and B) is indicated that excludes OPEX and VAT.

Source: Nikoliers

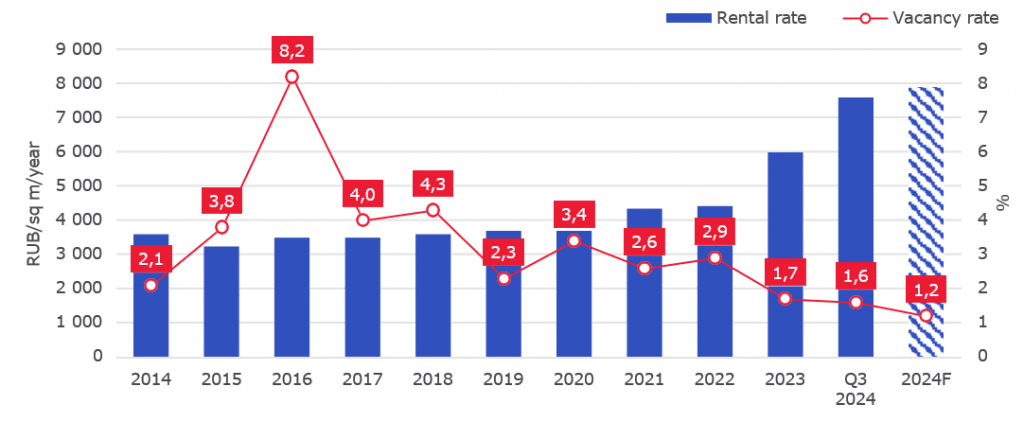

VACANCY AND RENTAL RATES: Saint Petersburg and Leningrad Region

In the Saint Petersburg and Leningrad Region market the vacancy rate remained at the level of the previous quarter at 0.7% or 37,000 sq m.

The weighted average base rent in class A facilities almost has not changed versus the previous quarter. However, amid the notable shortage of storage premises as well as the rapid absorption of high-quality offers in off-plan projects, we see explosive growth of the rental rate in B-class premises, where the rent stabilized at the level of RUB 9,650 per sq m per year, which means a 41% growth versus the end of 2023.

Dynamics of the weighted average rental rate* by classes and vacancy rate

VACANCY AND RENTAL RATES: Russian regions

In the regional industrial real estate market of Russia total vacant space, based on the results for Q3 2024, amounted to 226,000 sq m, of which class B premises account for 75%.

In a number of cities there is almost no vacant space on offer in A-class facilities with many developers giving preference to the BTS format over speculative construction in view of higher reliability and stability of this type of development projects.

Depending on the characteristics and age of a project, the weighted average base rent in move-in ready A-class facilities is in the range of 7-12 thousand RUB/sq m/year.

Dynamics of the weighted average rent* and vacancy rate

*The weighted average rent for move-in ready vacant dry warehouse premises (classes A and B) is indicated that excludes OPEX and VAT.

Source: Nikoliers

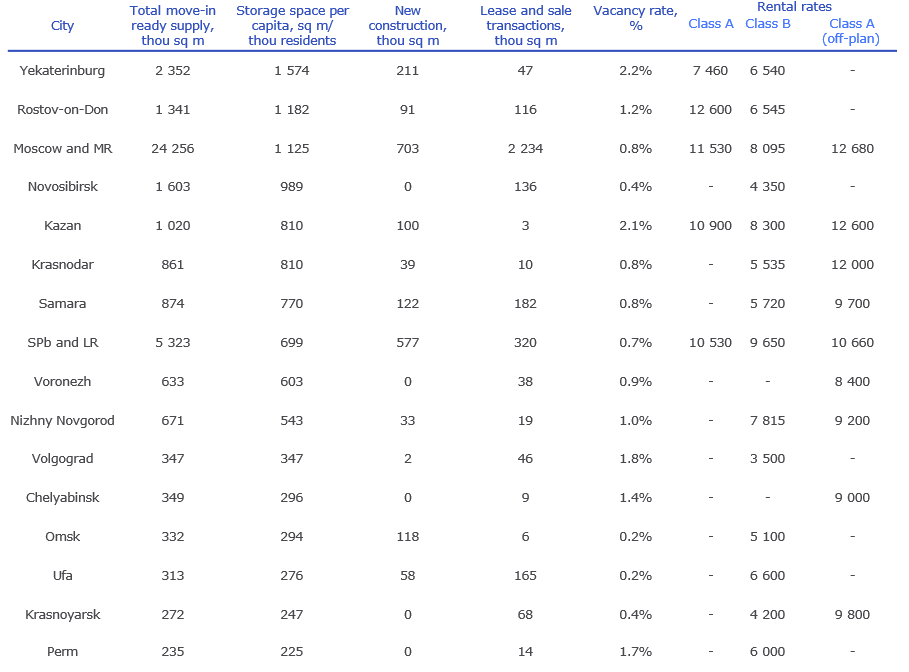

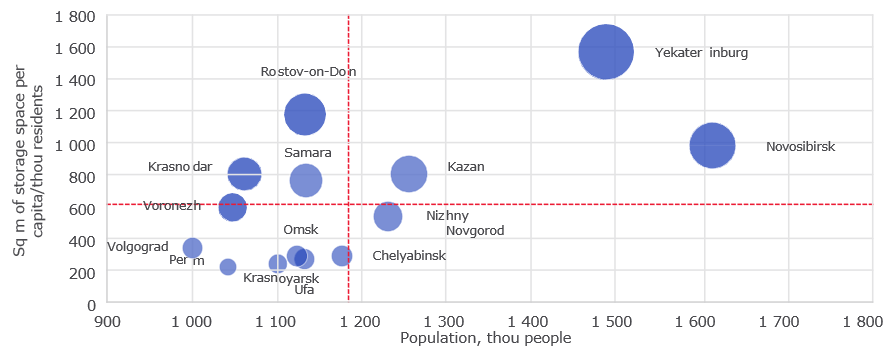

MAIN INDICATORS FOR THE MARKETS OF MILLION-PLUS CITIES

The following big cities of Russia are leaders in terms of warehouse space per 1,000 residents based on the results for Q3 2024: Yekaterinburg (1,574 sq m/thou people), Rostov-on-Don (1,182 sq m/thou people) and the Moscow area (1,125 sq m/thou people).

Nizhny Novgorod stands out among other million-plus cities in that its per capita storage space is below the average, specifically 543 sq m/thou people, even though its population is larger than average in the sample. This may signal a shortage of storage facilities in this region.

Comparing million-plus cities (without Moscow and Saint Petersburg) by quality industrial real estate per capita (the circle size reflecting the move-in ready supply of storage space)

*The weighted average rent for move-in ready vacant dry warehouse premises (classes A and B) is indicated that excludes OPEX and VAT.

Source: Nikoliers

LIGHT INDUSTRIAL MARKET

As of today, the total move-in ready supply of light industrial facilities in Russia comes to 739,000 sq m, of which 88% falls to the share of the Moscow area, 7% to the share of Saint Petersburg and Leningrad Region and 5% to the share of other Russian regions.

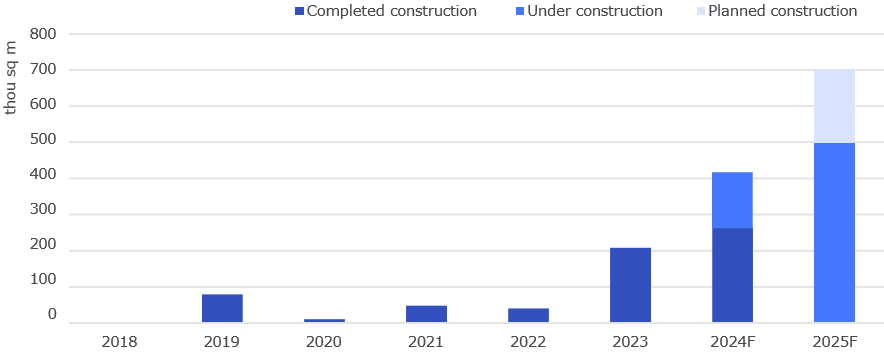

At the end of 2024, the LI supply in Russia, provided all planned projects are commissioned, may reach 934,000 sq m. It should be noted that this year first LI projects have already been commissioned in the regional markets of Yaroslavl and Krasnodar.

Dynamics of the announced commissioning of LI space

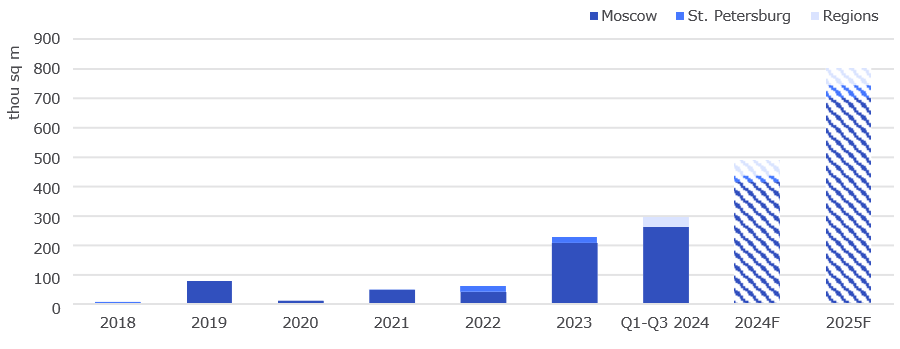

LIGHT INDUSTRIAL: Moscow and Moscow Region

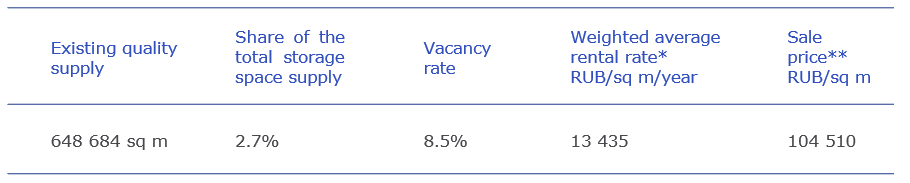

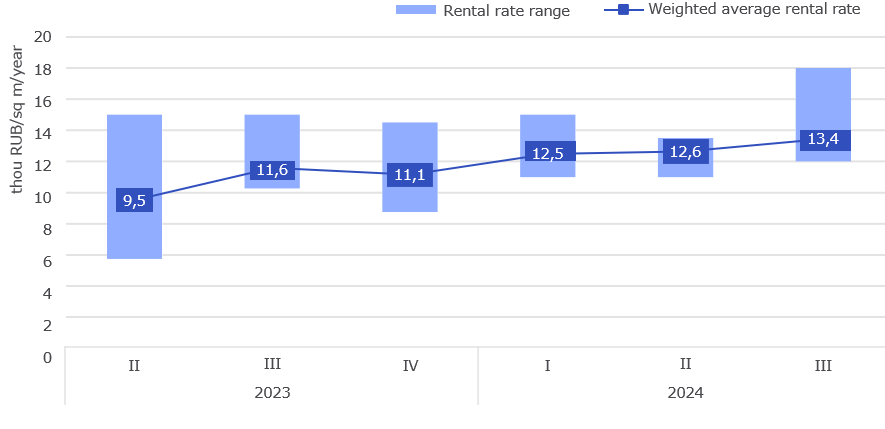

For nine months, more than 260,000 sq m of light industrial space was commissioned in Moscow and in the Moscow Region. Thus, the amount of move-in ready supply has risen to 649,000 sq m.The weighted average base rent for move-in ready and off-plan LI units has grown by 16% YoY to RUB 13,430 per sq m per year. The sale price rose by 25% versus the same period to RUB 104,510 per sq m.

Dynamics of the commissioning of LI projects

Source: Nikoliers

Key indicators for LI market (Moscow and the Moscow Region)

The range of rental rates* in light industrial facilities

The range of sale prices** for light industrial facilities

**Excluding VAT (20%) — for move-in ready and off-plan projects; weighted average indicator

Source: Nikoliers

LIGHT INDUSTRIAL: Saint Petersburg and Leningrad Region

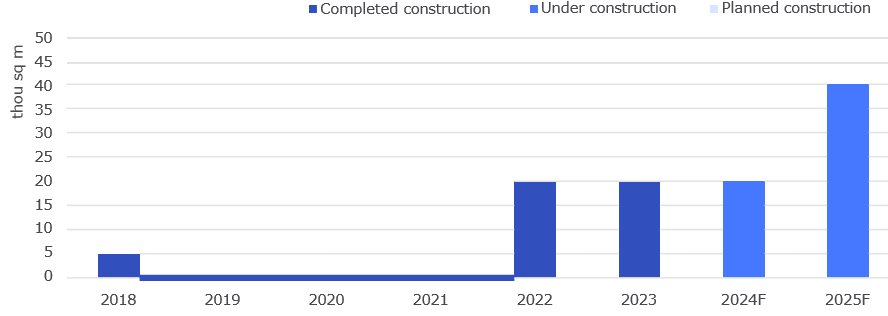

The Saint Petersburg LI market ranks second in size in Russia with total move-in ready supply standing at 55,000 sq m, which represents 1.0% of the total move-in ready quality storage space supply in the metro area. The total of 114,400 sq m are expected to be commissioned in 2024-2026.

The commercial terms in move-in ready and off-plan light industrial premises did not see any significant changes in the region vesus the previous quarter: the base rent stabilized at the level of 13,140 RUB/sq m/year, whereas the sale price stood at 114,780 RUB/sq m.

The dynamics of commissioning for LI projects

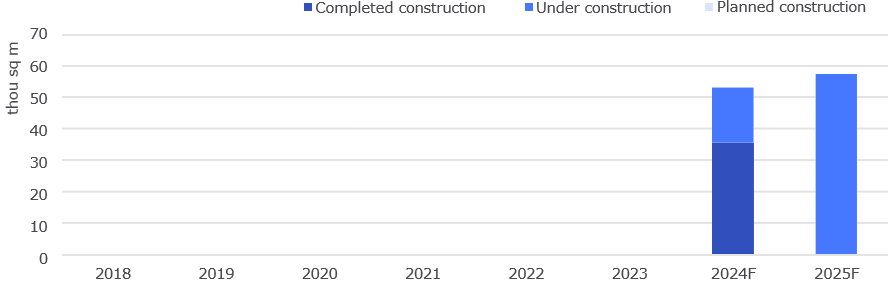

LIGHT INDUSTRIAL: Russian regions

For the past quarter first light industrial facilities were commissioned in the industrial real estate market of Russia, including an LI facility in Karabikhsky rural settlement (5,974 sq m, Yaroslavl Region) and LI Terminal facility (29,650 sq m in Krasnodar). Both facilities represent freestanding buildings with the floor space of 1,500 sq m each.

Till the year’s end the commissioning of two buildings in the earlier mentioned project in Yaroslavl Region is anticipated, in addition to an LI facility in the city of Chelyabinsk with the total floor area of about 14,500 sq m.

The dynamics of commissioning of LI projects

**Excluding VAT (20%) — for move-in ready and off-plan projects; weighted average indicator

Source: Nikoliers

TRENDS AND FORECAST

Maximum investment in the warehousing segment

For the nine months of 2024, investments in the warehousing segment amounted to RUB 116 billion, which is a historic maximum for this segment for the entire history of capital markets, almost twice exceeding the investment in this segment for the whole year 2023.And whereas in 10 recent years the average of three transactions worth more than RUB 1 billion were concluded in the warehousing segment, in Q3 2024 a record 14 of such deals were signed.

The reason for the given drastic increase in this indicator is a higher activity of closed- end MIFs and near-banking structures which, in addition to move-in ready facilities, started buying off-plan projects which have already been contracted for a long time ahead. The interest is keen not only on classic big-box formats, but also on LI facilities.

Testing new approaches to rental rate indexation

Developers, confronted with rapid and unpredictable changes on the market and in the national economy, are testing new approaches to the rent indexation. This is their natural response to the need of adaptation to market volatility, given that traditional methods of rent calculation are no longer reliable enough to protect the interests of developers from unforeseen economic shocks.Thus, a number of companies are developing an approach whereby the rental rate and its indexation is calculated proceeding from the Bank of Russia’s key interest rate. This approach will potentially allow the developer greater flexibility in responding to changes in the monetary and lending policy, which will be instrumental in the better management of financial risks and will bolster the competitiveness of projects on the market.

Victor Afanasenko, Regional Director Warehousing, Industrial Real Estate and Land Department:"In recent years the Russian industrial real estate market has undergone remarkable changes and it is currently faced with a number of challenges that need to be adressed in the foreseeable future. One of the main and grievous problems is the imbalance between demand and supply. We expect that in 2024 the explosive business activity will again exceed the 6-million-sqm mark, although only about 5.3 million sq m of new space will be commissioned. Thus, the new supply fails to catch up with demand again, which leads to the buildup of pent-up demand pushing up the rental rates and speeding up the absorption of new offers. What’s more, construction and debt financing costs remain high, which curbs the developer activity, especially as regards large-size speculative projects. The Bank of Russia’s average key interest rate is expected to remain higher than 15% next year, which will result in the slowdown of construction rates and will curtail the expediency of delivering large-sized projects. The market is getting increasingly attractive for players of different profiles and capital stocks. We see private equity investors turning their eyes to the Light Industrial format more often, whereas large companies, including residential developers, continue announcing major projects, especially in the Moscow area, including thanks to preferential integrated development and employment opportunities programs."

KEY INDICATORS OF RUSSIA’S MAIN MARKETS

*The weighted average rental rate for move-in

ready dry warehouse premises (of classes A and B) is indicated, excluding OPEX and VAT. For the Saint Petersburg industrial

real estate market the rental rate for

A-class premises is quoted.